커뮤니티

문의드립니다.

2019-07-04 08:14:18

347

글번호 130019

첨부 이미지

그림1

그림2

도움주시는 덕분에 도전하고 있습니다. 매번 감사합니다.

1 .기타

이 수식이요. 앞의 질문 2번 수식인데요. 본 수식은 해당 레인지 돌파하면 그 방향 진입하는 거고 수정 요청 드린 건 이전 진입이 수익이면 앞선 진입과 반대 방향 진입, 이전 진입이 손실이면 수식대로 진입하는 내용인데

실행해보니 그냥 이전이 수익이더라도 그 방향으로 가고 아니어도 그 방향으로 가는 것 같습니다.

Inputs: InitMin(90);

Variables: SessStartMin(0), TradeTime(0), SetHigh(0), SetLow(0), LongFlag(False), ShortFlag(False);

#conversion of hour-based time to minute-based time

SessStartMin = TimeToMinutes(90000);

TradeTime = TimeToMinutes(sTime);

input : 진입횟수(1),손절률(1),익절률(1);

var : count(0),T1(0);

input : 진입시간(90000),제한시간(150000),청산시간(153400),특정수익(3);

var : Tcond(false),pl(0),ps(0);

SetStopLoss(손절률,PercentStop);

SetStopProfittarget(익절률,PercentStop);

if (sdate != sdate[1] and stime >= 청산시간) or

(sdate == sdate[1] and stime >= 청산시간 and stime[1] < 청산시간) then

{

Tcond = false;

if MarketPosition == 1 Then

exitlong();

if MarketPosition == -1 Then

ExitShort();

}

if (sdate != sdate[1] and stime >= 진입시간) or

(sdate == sdate[1] and stime >= 진입시간 and stime[1] < 진입시간) then

{

Tcond = true;

T1 = TotalTrades;

}

if (sdate != sdate[1] and stime >= 제한시간) or

(sdate == sdate[1] and stime >= 제한시간 and stime[1] < 제한시간) then

{

Tcond = false;

}

if MarketPosition == 0 Then

count = TotalTrades-T1;

Else

count = TotalTrades-T1+1;

if Count < 진입횟수 and Tcond == true then

{

#Setup - establishment of the initial range

If TradeTime <= SessStartMin + InitMin Then

{

If Date <> Date[1] Then

{

SetHigh = High;

SetLow = Low;

LongFlag = True;

ShortFlag = True;

}

Else

{

If High > SetHigh Then

SetHigh = High;

If Low < SetLow Then

SetLow = Low;

}

}

Else

{

#Entries once the initial period has ended

if MarketPosition == 0 Then

{

pl = PositionProfit(1);

ps = MarketPosition(1);

}

Else

{

pl = PositionProfit(0);

ps = MarketPosition(0);

}

If LongFlag AND CrossUp( Close , SetHigh) Then

{

if pl <= 0 or (PL > 0 and ps != 1) Then

Buy();

}

If ShortFlag AND CrossDown(Close , SetLow) Then

{

if pl <= 0 or (pl > 0 and ps != -1) then

Sell();

}

}

}

#Long Protective Exit

If MarketPosition == 1 Then

{

LongFlag = False;

ExitLong("",atstop,SetLow );

ExitLong("BS",atlimit,EntryPrice+특정수익 );

}

#Short Protective Exit

If MarketPosition == -1 Then

{

ShortFlag = False;

ExitShort("",atstop,SetHigh );

ExitShort("SB",atlimit,EntryPrice-특정수익 );

}

input: TsValue(80);

var: Hvalue(0),Lvalue(0);

If MarketPosition() == 1 Then {

Hvalue = Highest(H,BarsSinceEntry+1);

ExitLong("trailstop_EL", Atstop, Hvalue-TsValue*PriceScale);

}

If MarketPosition() == -1 Then {

Lvalue = Lowest(L,BarsSinceEntry+1);

ExitShort("trailStop_Es", Atstop, Lvalue + TsValue*PriceScale);

}

2.

궁금해서 그러는데요. 작성해주신 2번 전략은 정확히 어떻게 작동하는 건가요? 본 전략이랑 성과가 다르긴 한 것 같은데 차트만 봐서는 뭐가 다른지 잘 모르겠습니다.

if pl <= 0 or (PL > 0 and ps != 1) Then

Buy();

여기로 이전 수익이랑 마켓 포지션 나누어 놓은 것 같기는 한데요. 정확히 어떻게 작동하는지 궁금합니다.

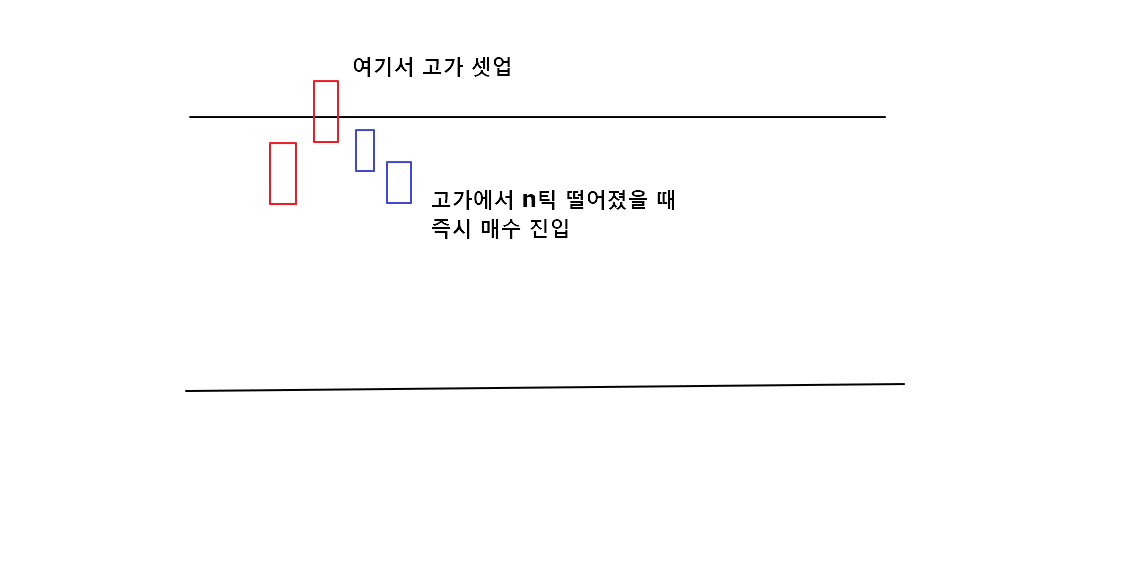

3. 앞선 질문의 3번 전략도요. 제가 보기엔 진입횟수도 적고 뭔가 제가 생각한 방향으로 안 나왔습니다. 첨부파일 2와 같은 것처럼 진입하게 하고 싶었거든요.

4. 1번 수식도 본수식(특정시간 인트라데이 돌파전략)의 매수 매도 조건을 만약 이전 수익이 특정 수익이상일 때 반대로 (원래 buy 수식이면 sell로, 그러니까 원래는 정방향 진입인데 특정 수익이 발생한 다음 매매에서는 역방향 진입)하는 거였는데 트레일링 스탑에만 있네요.

글로 어설프게 쓰다보니 설명을 잘 못하는 듯 합니다. 수식 도움 좀 부탁드립니다.

- 1. 130627_이미지_2.png (0.07 MB)

- 2. 130628_이미지_3.png (0.01 MB)

{kind=link}

{kind=link}

답변 1

예스스탁 예스스탁 답변

2019-07-04 10:46:12

안녕하세요

예스스탁입니다.

1

Inputs: InitMin(90);

Variables: SessStartMin(0), TradeTime(0), SetHigh(0), SetLow(0), LongFlag(False), ShortFlag(False);

#conversion of hour-based time to minute-based time

SessStartMin = TimeToMinutes(90000);

TradeTime = TimeToMinutes(sTime);

input : 진입횟수(1),손절률(1),익절률(1);

var : count(0),T1(0);

input : 진입시간(90000),제한시간(150000),청산시간(153400),특정수익(3);

var : Tcond(false),pl(0),ps(0);

SetStopLoss(손절률,PercentStop);

SetStopProfittarget(익절률,PercentStop);

if (sdate != sdate[1] and stime >= 청산시간) or

(sdate == sdate[1] and stime >= 청산시간 and stime[1] < 청산시간) then

{

Tcond = false;

if MarketPosition == 1 Then

exitlong();

if MarketPosition == -1 Then

ExitShort();

}

if (sdate != sdate[1] and stime >= 진입시간) or

(sdate == sdate[1] and stime >= 진입시간 and stime[1] < 진입시간) then

{

Tcond = true;

T1 = TotalTrades;

}

if (sdate != sdate[1] and stime >= 제한시간) or

(sdate == sdate[1] and stime >= 제한시간 and stime[1] < 제한시간) then

{

Tcond = false;

}

if MarketPosition == 0 Then

count = TotalTrades-T1;

Else

count = TotalTrades-T1+1;

if Count < 진입횟수 and Tcond == true then

{

#Setup - establishment of the initial range

If TradeTime <= SessStartMin + InitMin Then

{

If Date <> Date[1] Then

{

SetHigh = High;

SetLow = Low;

LongFlag = True;

ShortFlag = True;

}

Else

{

If High > SetHigh Then

SetHigh = High;

If Low < SetLow Then

SetLow = Low;

}

}

Else

{

#Entries once the initial period has ended

if MarketPosition == 0 Then

{

pl = PositionProfit(1);

ps = MarketPosition(1);

}

Else

{

pl = PositionProfit(0);

ps = MarketPosition(0);

}

If LongFlag AND CrossUp( Close , SetHigh) Then

{

if pl <= 0 Then

Buy();

Else

sell();

}

If ShortFlag AND CrossDown(Close , SetLow) Then

{

if pl <= 0 then

Sell();

Else

buy();

}

}

}

#Long Protective Exit

If MarketPosition == 1 Then Begin

LongFlag = False;

ExitLong("",atstop,SetLow );

sell("BS",atlimit,EntryPrice+특정수익 );

End;

#Short Protective Exit

If MarketPosition == -1 Then Begin

ShortFlag = False;

ExitShort("",atstop,SetHigh );

buy("SB",atlimit,EntryPrice-특정수익 );

End;

input: TsValue(80);

var: Hvalue(0),Lvalue(0);

If MarketPosition() == 1 Then {

Hvalue = Highest(H,BarsSinceEntry+1);

ExitLong("trailstop_EL", Atstop, Hvalue-TsValue*PriceScale);

}

If MarketPosition() == -1 Then {

Lvalue = Lowest(L,BarsSinceEntry+1);

ExitShort("trailStop_Es", Atstop, Lvalue + TsValue*PriceScale);

}

2

이전 답변드린 수식에 보시며 아래 내용이 있습니다.

if MarketPosition == 0 Then

{

pl = PositionProfit(1);

ps = MarketPosition(1);

}

Else

{

pl = PositionProfit(0);

ps = MarketPosition(0);

}

현재 무포지션이면 pl에 진전거래의 손익을, ps에는 포지션 방향을 저장합니다.

현재 포지션진행중이면(스위칭될 경우 대비) pl에는 현재 진행중인 거래의 손익을

ps에는 현재 포지션의 방향을 저장합니다.

이후에

If LongFlag AND CrossUp( Close , SetHigh) Then

{

if pl <= 0 or (PL > 0 and ps != 1) Then

Buy();

}

If ShortFlag AND CrossDown(Close , SetLow) Then

{

if pl <= 0 or (pl > 0 and ps != -1) then

Sell();

}

매수조건 충족시에 pl이 0이하(손실) 이거나 수익이면 직전거래가 반대방향일때만 매수진입

매수조건 충족시에 pl이 0이하(손실) 이거나 수익이면 직전거래가 반대방향일때만 매도진입

하는 내용이었습니다. 직전거래 포지션과 손익에 따라 매수나 매도진입을 할것인가 말것인가를 지정한 내용이었습니다.

3

기존2번식에 해당 내용을 추가했습니다.

1번식에 해당 내용을 추가했습니다.

Inputs: InitMin(90);

Variables: SessStartMin(0), TradeTime(0), SetHigh(0), SetLow(0), LongFlag(False), ShortFlag(False);

#conversion of hour-based time to minute-based time

SessStartMin = TimeToMinutes(90000);

TradeTime = TimeToMinutes(sTime);

input : 진입횟수(1),손절률(1),익절률(1);

var : count(0),T1(0);

input : 진입시간(90000),제한시간(150000),청산시간(153400),특정수익(3),n(5);

var : Tcond(false),pl(0),ps(0),T(0),S(0);

SetStopLoss(손절률,PercentStop);

SetStopProfittarget(익절률,PercentStop);

if (sdate != sdate[1] and stime >= 청산시간) or

(sdate == sdate[1] and stime >= 청산시간 and stime[1] < 청산시간) then

{

Tcond = false;

if MarketPosition == 1 Then

exitlong();

if MarketPosition == -1 Then

ExitShort();

}

if (sdate != sdate[1] and stime >= 진입시간) or

(sdate == sdate[1] and stime >= 진입시간 and stime[1] < 진입시간) then

{

Tcond = true;

T1 = TotalTrades;

}

if (sdate != sdate[1] and stime >= 제한시간) or

(sdate == sdate[1] and stime >= 제한시간 and stime[1] < 제한시간) then

{

Tcond = false;

}

if MarketPosition == 0 Then

count = TotalTrades-T1;

Else

count = TotalTrades-T1+1;

if Count < 진입횟수 and Tcond == true then

{

#Setup - establishment of the initial range

If TradeTime <= SessStartMin + InitMin Then

{

If Date <> Date[1] Then

{

SetHigh = High;

SetLow = Low;

LongFlag = True;

ShortFlag = True;

}

Else

{

If High > SetHigh Then

SetHigh = High;

If Low < SetLow Then

SetLow = Low;

}

}

Else

{

#Entries once the initial period has ended

if MarketPosition == 0 Then

{

pl = PositionProfit(1);

ps = MarketPosition(1);

}

Else

{

pl = PositionProfit(0);

ps = MarketPosition(0);

}

If LongFlag AND CrossUp( Close , SetHigh) Then

{

T = 1;

S = H-PriceScale*n;

}

If ShortFlag AND CrossDown(Close , SetLow) Then

{

T = -1;

S = L-PriceScale*n;

}

if T == 1 Then

Buy("b",atlimit,S);

if T == -1 Then

sell("s",atlimit,S);

}

}

#Long Protective Exit

If MarketPosition == 1 Then Begin

LongFlag = False;

ExitLong("",atstop,SetLow );

sell("BS",atlimit,EntryPrice+특정수익 );

End;

#Short Protective Exit

If MarketPosition == -1 Then Begin

ShortFlag = False;

ExitShort("",atstop,SetHigh );

buy("SB",atlimit,EntryPrice-특정수익 );

End;

input: TsValue(80);

var: Hvalue(0),Lvalue(0);

If MarketPosition() == 1 Then {

Hvalue = Highest(H,BarsSinceEntry+1);

ExitLong("trailstop_EL", Atstop, Hvalue-TsValue*PriceScale);

}

If MarketPosition() == -1 Then {

Lvalue = Lowest(L,BarsSinceEntry+1);

ExitShort("trailStop_Es", Atstop, Lvalue + TsValue*PriceScale);

}

4

1번 수식의 일정수익시 반대방향 진입이 청산으로 되어 있어 수정했습니다.

Inputs: InitMin(90);

Variables: SessStartMin(0), TradeTime(0), SetHigh(0), SetLow(0), LongFlag(False), ShortFlag(False);

#conversion of hour-based time to minute-based time

SessStartMin = TimeToMinutes(90000);

TradeTime = TimeToMinutes(sTime);

input : 진입횟수(1),손절률(1),익절률(1);

var : count(0),T1(0);

input : 진입시간(90000),제한시간(150000),청산시간(153400),특정수익(3);

var : Tcond(false);

SetStopLoss(손절률,PercentStop);

SetStopProfittarget(익절률,PercentStop);

if (sdate != sdate[1] and stime >= 청산시간) or

(sdate == sdate[1] and stime >= 청산시간 and stime[1] < 청산시간) then

{

Tcond = false;

if MarketPosition == 1 Then

exitlong();

if MarketPosition == -1 Then

ExitShort();

}

if (sdate != sdate[1] and stime >= 진입시간) or

(sdate == sdate[1] and stime >= 진입시간 and stime[1] < 진입시간) then

{

Tcond = true;

T1 = TotalTrades;

}

if (sdate != sdate[1] and stime >= 제한시간) or

(sdate == sdate[1] and stime >= 제한시간 and stime[1] < 제한시간) then

{

Tcond = false;

}

if MarketPosition == 0 Then

count = TotalTrades-T1;

Else

count = TotalTrades-T1+1;

if Count < 진입횟수 and Tcond == true then

{

#Setup - establishment of the initial range

If TradeTime <= SessStartMin + InitMin Then

{

If Date <> Date[1] Then

{

SetHigh = High;

SetLow = Low;

LongFlag = True;

ShortFlag = True;

}

Else

{

If High > SetHigh Then

SetHigh = High;

If Low < SetLow Then

SetLow = Low;

}

}

Else

{

#Entries once the initial period has ended

If LongFlag AND CrossUp( Close , SetHigh) Then

{

Buy();

}

If ShortFlag AND CrossDown(Close , SetLow) Then

{

Sell();

}

}

}

#Long Protective Exit

If MarketPosition == 1 Then Begin

LongFlag = False;

ExitLong("",atstop,SetLow );

sell("BS",atlimit,EntryPrice+특정수익 );

End;

#Short Protective Exit

If MarketPosition == -1 Then Begin

ShortFlag = False;

ExitShort("",atstop,SetHigh );

buy("SB",atlimit,EntryPrice-특정수익 );

End;

input: TsValue(80);

var: Hvalue(0),Lvalue(0);

If MarketPosition() == 1 Then {

Hvalue = Highest(H,BarsSinceEntry+1);

ExitLong("trailstop_EL", Atstop, Hvalue-TsValue*PriceScale);

}

If MarketPosition() == -1 Then {

Lvalue = Lowest(L,BarsSinceEntry+1);

ExitShort("trailStop_Es", Atstop, Lvalue + TsValue*PriceScale);

}

즐거운 하루되세요

> 잡다백수 님이 쓴 글입니다.

> 제목 : 문의드립니다.

> 도움주시는 덕분에 도전하고 있습니다. 매번 감사합니다.

1 .기타

이 수식이요. 앞의 질문 2번 수식인데요. 본 수식은 해당 레인지 돌파하면 그 방향 진입하는 거고 수정 요청 드린 건 이전 진입이 수익이면 앞선 진입과 반대 방향 진입, 이전 진입이 손실이면 수식대로 진입하는 내용인데

실행해보니 그냥 이전이 수익이더라도 그 방향으로 가고 아니어도 그 방향으로 가는 것 같습니다.

Inputs: InitMin(90);

Variables: SessStartMin(0), TradeTime(0), SetHigh(0), SetLow(0), LongFlag(False), ShortFlag(False);

#conversion of hour-based time to minute-based time

SessStartMin = TimeToMinutes(90000);

TradeTime = TimeToMinutes(sTime);

input : 진입횟수(1),손절률(1),익절률(1);

var : count(0),T1(0);

input : 진입시간(90000),제한시간(150000),청산시간(153400),특정수익(3);

var : Tcond(false),pl(0),ps(0);

SetStopLoss(손절률,PercentStop);

SetStopProfittarget(익절률,PercentStop);

if (sdate != sdate[1] and stime >= 청산시간) or

(sdate == sdate[1] and stime >= 청산시간 and stime[1] < 청산시간) then

{

Tcond = false;

if MarketPosition == 1 Then

exitlong();

if MarketPosition == -1 Then

ExitShort();

}

if (sdate != sdate[1] and stime >= 진입시간) or

(sdate == sdate[1] and stime >= 진입시간 and stime[1] < 진입시간) then

{

Tcond = true;

T1 = TotalTrades;

}

if (sdate != sdate[1] and stime >= 제한시간) or

(sdate == sdate[1] and stime >= 제한시간 and stime[1] < 제한시간) then

{

Tcond = false;

}

if MarketPosition == 0 Then

count = TotalTrades-T1;

Else

count = TotalTrades-T1+1;

if Count < 진입횟수 and Tcond == true then

{

#Setup - establishment of the initial range

If TradeTime <= SessStartMin + InitMin Then

{

If Date <> Date[1] Then

{

SetHigh = High;

SetLow = Low;

LongFlag = True;

ShortFlag = True;

}

Else

{

If High > SetHigh Then

SetHigh = High;

If Low < SetLow Then

SetLow = Low;

}

}

Else

{

#Entries once the initial period has ended

if MarketPosition == 0 Then

{

pl = PositionProfit(1);

ps = MarketPosition(1);

}

Else

{

pl = PositionProfit(0);

ps = MarketPosition(0);

}

If LongFlag AND CrossUp( Close , SetHigh) Then

{

if pl <= 0 or (PL > 0 and ps != 1) Then

Buy();

}

If ShortFlag AND CrossDown(Close , SetLow) Then

{

if pl <= 0 or (pl > 0 and ps != -1) then

Sell();

}

}

}

#Long Protective Exit

If MarketPosition == 1 Then

{

LongFlag = False;

ExitLong("",atstop,SetLow );

ExitLong("BS",atlimit,EntryPrice+특정수익 );

}

#Short Protective Exit

If MarketPosition == -1 Then

{

ShortFlag = False;

ExitShort("",atstop,SetHigh );

ExitShort("SB",atlimit,EntryPrice-특정수익 );

}

input: TsValue(80);

var: Hvalue(0),Lvalue(0);

If MarketPosition() == 1 Then {

Hvalue = Highest(H,BarsSinceEntry+1);

ExitLong("trailstop_EL", Atstop, Hvalue-TsValue*PriceScale);

}

If MarketPosition() == -1 Then {

Lvalue = Lowest(L,BarsSinceEntry+1);

ExitShort("trailStop_Es", Atstop, Lvalue + TsValue*PriceScale);

}

2.

궁금해서 그러는데요. 작성해주신 2번 전략은 정확히 어떻게 작동하는 건가요? 본 전략이랑 성과가 다르긴 한 것 같은데 차트만 봐서는 뭐가 다른지 잘 모르겠습니다.

if pl <= 0 or (PL > 0 and ps != 1) Then

Buy();

여기로 이전 수익이랑 마켓 포지션 나누어 놓은 것 같기는 한데요. 정확히 어떻게 작동하는지 궁금합니다.

3. 앞선 질문의 3번 전략도요. 제가 보기엔 진입횟수도 적고 뭔가 제가 생각한 방향으로 안 나왔습니다. 첨부파일 2와 같은 것처럼 진입하게 하고 싶었거든요.

4. 1번 수식도 본수식(특정시간 인트라데이 돌파전략)의 매수 매도 조건을 만약 이전 수익이 특정 수익이상일 때 반대로 (원래 buy 수식이면 sell로, 그러니까 원래는 정방향 진입인데 특정 수익이 발생한 다음 매매에서는 역방향 진입)하는 거였는데 트레일링 스탑에만 있네요.

글로 어설프게 쓰다보니 설명을 잘 못하는 듯 합니다. 수식 도움 좀 부탁드립니다.

다음글

이전글