커뮤니티

전략식 합치는거 가능할까요?

2021-03-01 12:57:41

1032

글번호 146709

첨부 이미지

그림1

그림2

그림3

그림4

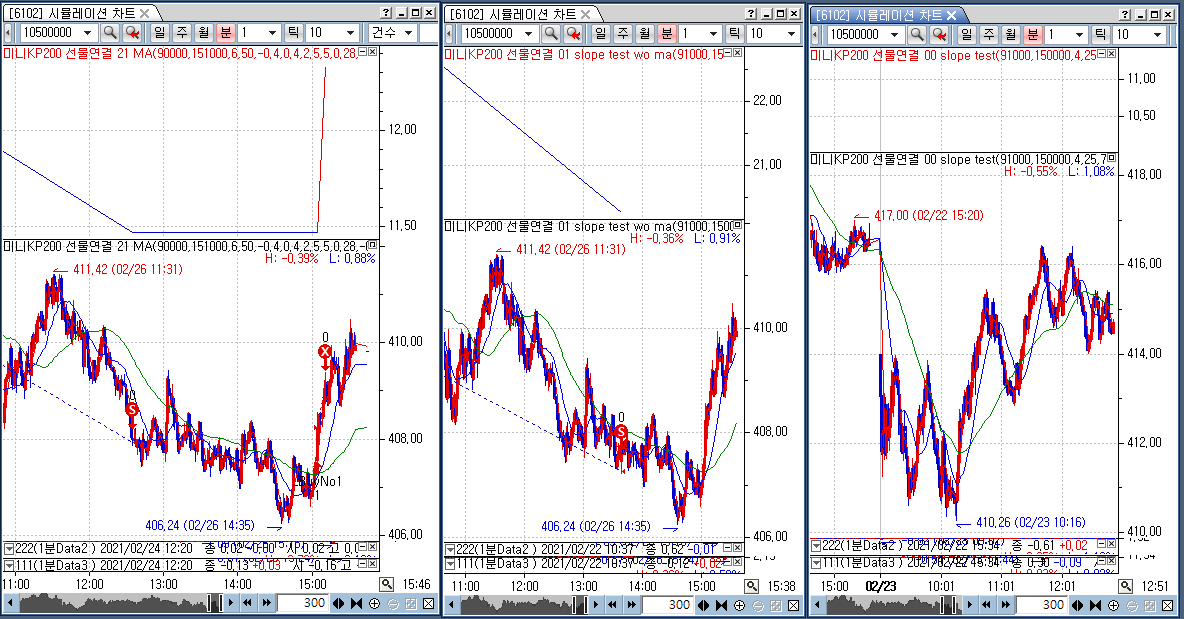

같은 엑셀 data를 쓰는 세개의 차트입니다.

너무 공간을 차지하고 예트가 너무 느려지는 요인이 됩니다.ㅜㅜ

시스템 합성 관리자 써보려고했는데 잘 안되네요..

피라미딩은아니고,

차트당 1개씩 진입/청산, 최대 동시 포지션은 3개진입이 되겠네요..

꼭 부탁합니다.

-----------------------------

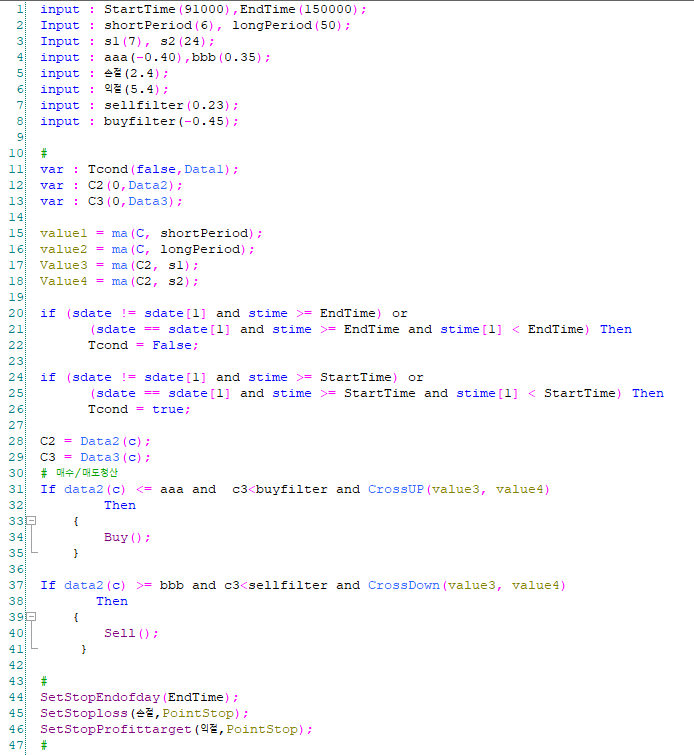

input : StartTime(90000),EndTime(151000);

Input : shortPeriod(6), longPeriod(50);

input : aaa(-0.40),bbb(0.40);

input : 손절(2.5);

input : 익절(5.0);

input : sellfilter(0.28);

input : buyfilter(-0.55);

var : Tcond(false,Data1);

var : C2(0,Data2);

var : C3(0,Data3);

value1 = ma(C, shortPeriod);

value2 = ma(C, longPeriod);

if (sdate != sdate[1] and stime >= EndTime) or

(sdate == sdate[1] and stime >= EndTime and stime[1] < EndTime) Then

Tcond = False;

if (sdate != sdate[1] and stime >= StartTime) or

(sdate == sdate[1] and stime >= StartTime and stime[1] < StartTime) Then

Tcond = true;

C2 = Data2(c);

C3 = Data3(c);

# 매수/매도청산

If data2(c) <= aaa and c3<buyfilter and CrossUP(value1, value2) Then

{

Buy();

}

If data2(c) >= bbb and c3<sellfilter and CrossDown(value1, value2) Then

{

Sell();

}

#

SetStopEndofday(EndTime);

SetStoploss(손절,PointStop);

SetStopProfittarget(익절,PointStop);

-------------------------------------------------------------

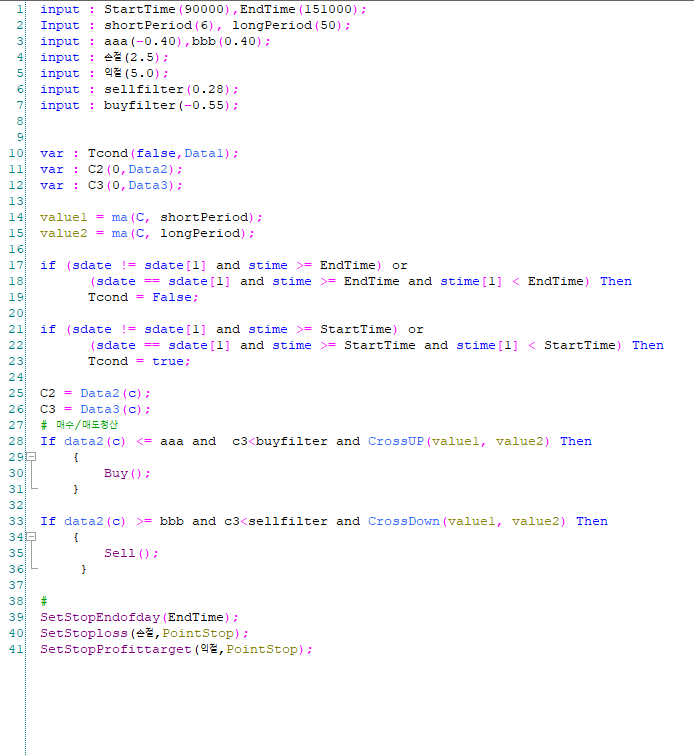

input : StartTime(91000),EndTime(150000);

Input : shortPeriod(6), longPeriod(50);

Input : s1(7), s2(24);

input : aaa(-0.40),bbb(0.35);

input : 손절(2.4);

input : 익절(5.4);

input : sellfilter(0.23);

input : buyfilter(-0.45);

var : Tcond(false,Data1);

var : C2(0,Data2);

var : C3(0,Data3);

value1 = ma(C, shortPeriod);

value2 = ma(C, longPeriod);

Value3 = ma(C2, s1);

Value4 = ma(C2, s2);

if (sdate != sdate[1] and stime >= EndTime) or

(sdate == sdate[1] and stime >= EndTime and stime[1] < EndTime) Then

Tcond = False;

if (sdate != sdate[1] and stime >= StartTime) or

(sdate == sdate[1] and stime >= StartTime and stime[1] < StartTime) Then

Tcond = true;

C2 = Data2(c);

C3 = Data3(c);

# 매수/매도청산

If data2(c) <= aaa and c3<buyfilter and CrossUP(value3, value4)

and CrossUP(value1, value2) Then

{

Buy();

}

If data2(c) >= bbb and c3<sellfilter and CrossDown(value3, value4)

and CrossDown(value1, value2) Then

{

Sell();

}

#

SetStopEndofday(EndTime);

SetStoploss(손절,PointStop);

SetStopProfittarget(익절,PointStop);

----------------------------------------------------------------------

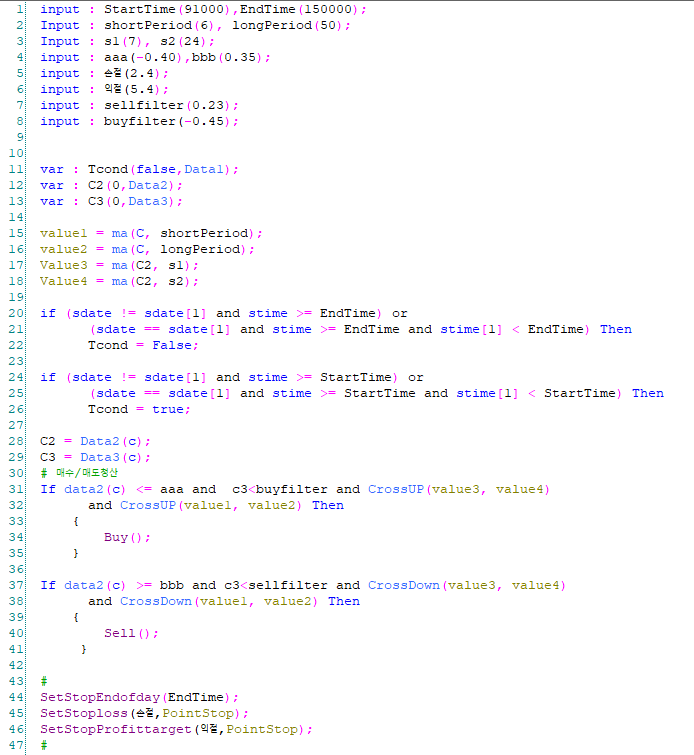

input : StartTime(91000),EndTime(150000);

Input : shortPeriod(6), longPeriod(50);

Input : s1(7), s2(24);

input : aaa(-0.40),bbb(0.35);

input : 손절(2.4);

input : 익절(5.4);

input : sellfilter(0.23);

input : buyfilter(-0.45);

#

var : Tcond(false,Data1);

var : C2(0,Data2);

var : C3(0,Data3);

value1 = ma(C, shortPeriod);

value2 = ma(C, longPeriod);

Value3 = ma(C2, s1);

Value4 = ma(C2, s2);

if (sdate != sdate[1] and stime >= EndTime) or

(sdate == sdate[1] and stime >= EndTime and stime[1] < EndTime) Then

Tcond = False;

if (sdate != sdate[1] and stime >= StartTime) or

(sdate == sdate[1] and stime >= StartTime and stime[1] < StartTime) Then

Tcond = true;

C2 = Data2(c);

C3 = Data3(c);

# 매수/매도청산

If data2(c) <= aaa and c3<buyfilter and CrossUP(value3, value4)

Then

{

Buy();

}

If data2(c) >= bbb and c3<sellfilter and CrossDown(value3, value4)

Then

{

Sell();

}

#

SetStopEndofday(EndTime);

SetStoploss(손절,PointStop);

SetStopProfittarget(익절,PointStop);

- 1. 캡처_2021_03_01_12_51_33_152.png (0.04 MB)

- 2. 캡처_2021_03_01_12_51_50_828.png (0.04 MB)

- 3. 캡처_2021_03_01_12_51_27_862.png (0.04 MB)

- 4. 캡처_2021_03_01_12_49_37_924.png (0.06 MB)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

답변 1

예스스탁 예스스탁 답변

2021-03-02 16:57:07

안녕하세요

예스스탁입니다.

문의하신 내용은 가능하지 않습니다.

기존 방법과 같이 각 차트에 적용해 사용하셔야 합니다.

3개의 시스템을 합쳐 하나의 시스템으로 만들면

각 전략별로 모두 별도로 신호가 발생하는 것이 아닙니다.

3개의 매수진입과 3개의 매도진입이 있는 하나의 시스템이 됩니다.

하나의 차트에서 발생하게 되므로 3개의 전략들의 매수 중 먼저만족한 것으로 매수진입

3개의 매도 중 먼저 만족한 것으로 청산하고 매도가 됩니다.

즉 각 다른전략의 진입과 청산으로 간섭이 발생하게 됩니다.

이것은 합성관리자로 만들어도 동일합니다.

즐거운 하루되세요

> 캣피쉬 님이 쓴 글입니다.

> 제목 : 전략식 합치는거 가능할까요?

> 같은 엑셀 data를 쓰는 세개의 차트입니다.

너무 공간을 차지하고 예트가 너무 느려지는 요인이 됩니다.ㅜㅜ

시스템 합성 관리자 써보려고했는데 잘 안되네요..

피라미딩은아니고,

차트당 1개씩 진입/청산, 최대 동시 포지션은 3개진입이 되겠네요..

꼭 부탁합니다.

-----------------------------

input : StartTime(90000),EndTime(151000);

Input : shortPeriod(6), longPeriod(50);

input : aaa(-0.40),bbb(0.40);

input : 손절(2.5);

input : 익절(5.0);

input : sellfilter(0.28);

input : buyfilter(-0.55);

var : Tcond(false,Data1);

var : C2(0,Data2);

var : C3(0,Data3);

value1 = ma(C, shortPeriod);

value2 = ma(C, longPeriod);

if (sdate != sdate[1] and stime >= EndTime) or

(sdate == sdate[1] and stime >= EndTime and stime[1] < EndTime) Then

Tcond = False;

if (sdate != sdate[1] and stime >= StartTime) or

(sdate == sdate[1] and stime >= StartTime and stime[1] < StartTime) Then

Tcond = true;

C2 = Data2(c);

C3 = Data3(c);

# 매수/매도청산

If data2(c) <= aaa and c3<buyfilter and CrossUP(value1, value2) Then

{

Buy();

}

If data2(c) >= bbb and c3<sellfilter and CrossDown(value1, value2) Then

{

Sell();

}

#

SetStopEndofday(EndTime);

SetStoploss(손절,PointStop);

SetStopProfittarget(익절,PointStop);

-------------------------------------------------------------

input : StartTime(91000),EndTime(150000);

Input : shortPeriod(6), longPeriod(50);

Input : s1(7), s2(24);

input : aaa(-0.40),bbb(0.35);

input : 손절(2.4);

input : 익절(5.4);

input : sellfilter(0.23);

input : buyfilter(-0.45);

var : Tcond(false,Data1);

var : C2(0,Data2);

var : C3(0,Data3);

value1 = ma(C, shortPeriod);

value2 = ma(C, longPeriod);

Value3 = ma(C2, s1);

Value4 = ma(C2, s2);

if (sdate != sdate[1] and stime >= EndTime) or

(sdate == sdate[1] and stime >= EndTime and stime[1] < EndTime) Then

Tcond = False;

if (sdate != sdate[1] and stime >= StartTime) or

(sdate == sdate[1] and stime >= StartTime and stime[1] < StartTime) Then

Tcond = true;

C2 = Data2(c);

C3 = Data3(c);

# 매수/매도청산

If data2(c) <= aaa and c3<buyfilter and CrossUP(value3, value4)

and CrossUP(value1, value2) Then

{

Buy();

}

If data2(c) >= bbb and c3<sellfilter and CrossDown(value3, value4)

and CrossDown(value1, value2) Then

{

Sell();

}

#

SetStopEndofday(EndTime);

SetStoploss(손절,PointStop);

SetStopProfittarget(익절,PointStop);

----------------------------------------------------------------------

input : StartTime(91000),EndTime(150000);

Input : shortPeriod(6), longPeriod(50);

Input : s1(7), s2(24);

input : aaa(-0.40),bbb(0.35);

input : 손절(2.4);

input : 익절(5.4);

input : sellfilter(0.23);

input : buyfilter(-0.45);

#

var : Tcond(false,Data1);

var : C2(0,Data2);

var : C3(0,Data3);

value1 = ma(C, shortPeriod);

value2 = ma(C, longPeriod);

Value3 = ma(C2, s1);

Value4 = ma(C2, s2);

if (sdate != sdate[1] and stime >= EndTime) or

(sdate == sdate[1] and stime >= EndTime and stime[1] < EndTime) Then

Tcond = False;

if (sdate != sdate[1] and stime >= StartTime) or

(sdate == sdate[1] and stime >= StartTime and stime[1] < StartTime) Then

Tcond = true;

C2 = Data2(c);

C3 = Data3(c);

# 매수/매도청산

If data2(c) <= aaa and c3<buyfilter and CrossUP(value3, value4)

Then

{

Buy();

}

If data2(c) >= bbb and c3<sellfilter and CrossDown(value3, value4)

Then

{

Sell();

}

#

SetStopEndofday(EndTime);

SetStoploss(손절,PointStop);

SetStopProfittarget(익절,PointStop);