커뮤니티

볼린저 밴드 수식 점검 문의드립니다.

2021-04-19 21:39:31

1686

글번호 148190

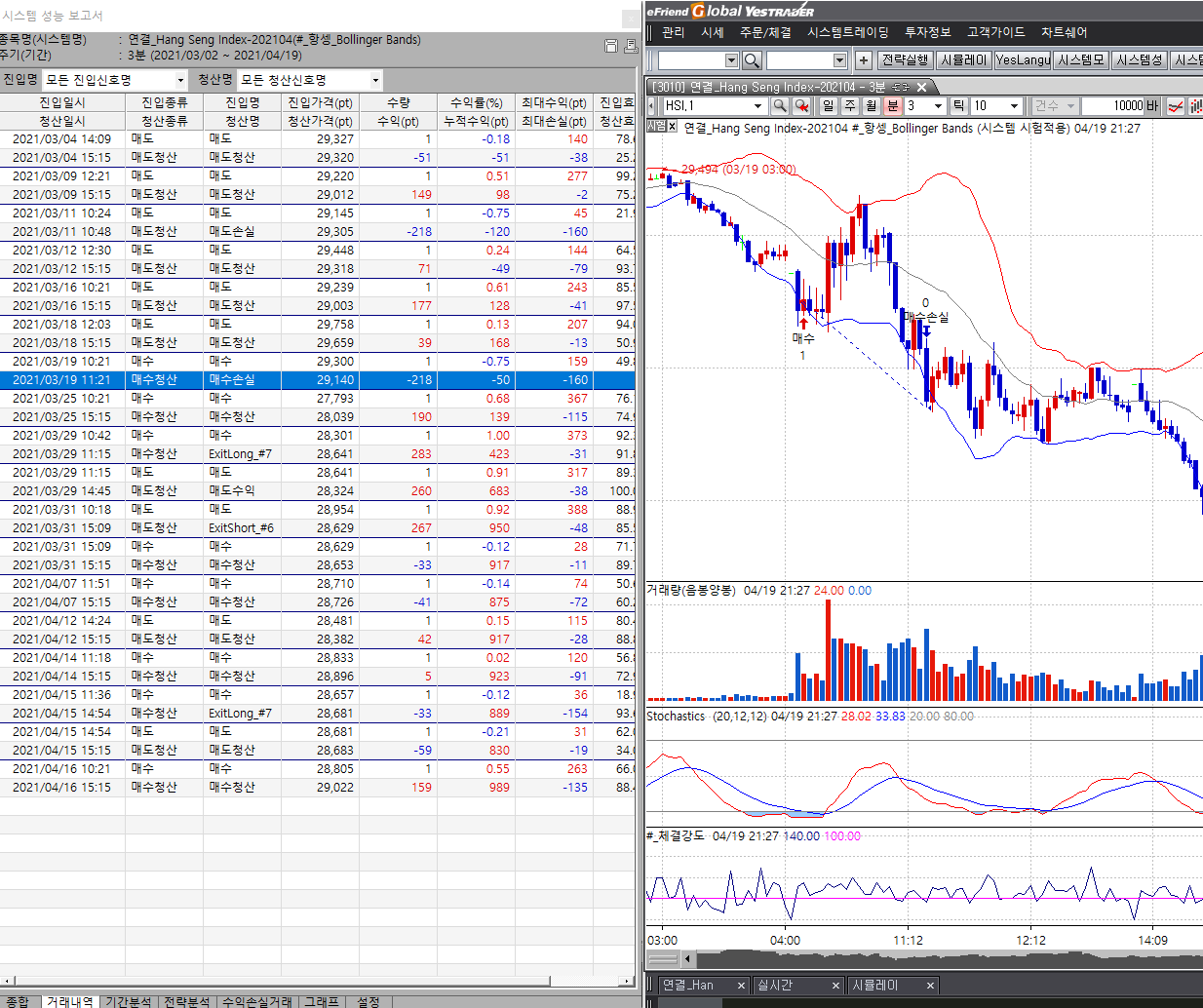

첨부 이미지

그림1

아래의 수식을 시뮬레이션 해보았습니다.

당일누적손실틱수를 160틱으로 잡아보았습니다.

그런데 160틱에서 손절되는게 아니고 봉이 완성될때까지 기다렸다가 시그널이 발생되는거 같습니다.

명령어를 Atstop으로 해서 당연히 되는줄 알았는데 아닌거 같아서요 ~

160틱에서 stop되게 하려면 무엇을 바꿔야 하는지 좀 알려주시면 감사하겠습니다.

- 아 래 -

Inputs: Length(9), StdDev(2), Bars(2);

Variables: BBTop(0),BBBot(0);

Input : 당일누적수익틱수(500),당일누적손실틱수(160);

input : starttime(100000),endtime(200000);

VARS: Tcond(false),N1(0),dayPl(0),당일누적수익(0),당일누적손실(0),Xcond(false),stok(0),stod(0);

if (sdate != sdate[1] and stime >= endtime) or

(sdate == sdate[1] and stime >= endtime and stime[1] < endtime) then

{

Tcond = false;

if MarketPosition == 1 Then

ExitLong("매수청산");

if MarketPosition == -1 Then

ExitShort("매도청산");

}

if (sdate != sdate[1] and stime >= starttime) or

(sdate == sdate[1] and stime >= starttime and stime[1] < starttime) then

{

Xcond = false;

N1 = NetProfit;

Tcond = true;

}

당일누적수익 = PriceScale*당일누적수익틱수;

당일누적손실 = PriceScale*당일누적손실틱수;

daypl = NetProfit-N1;

if TotalTrades > TotalTrades[1] then

{

if daypl >= 당일누적수익 or daypl <= -당일누적손실 Then

Xcond = true;

if (IsExitName("dbp",1) == true or IsExitName("dbl",1) == true or

IsExitName("dsp",1) == true or IsExitName("dsl",1) == true) then

Xcond = true;

}

if MarketPosition == 1 then{

ExitLong("매수수익",atlimit,EntryPrice+((당일누적수익-daypl)/CurrentContracts));

ExitLong("매수손실",AtStop,EntryPrice-((당일누적손실+daypl)/CurrentContracts));

}

if MarketPosition == -1 then{

ExitShort("매도수익",atlimit,EntryPrice-((당일누적수익-daypl)/CurrentContracts));

ExitShort("매도손실",AtStop,EntryPrice+((당일누적손실+daypl)/CurrentContracts));

}

BBTop = BollBandup(Length, StdDev);

BBBot = BollBanddown(Length, StdDev);

If Tcond == true and Xcond == False and CountIF(Close < BBBot, Bars) == Bars Then

Buy("매수", AtStop, BBBot);

If Tcond == true and Xcond == False and CountIF(Close > BBTop, Bars) == Bars Then

Sell("매도", AtStop, BBTop);

- 1. 148904_제목_없음.png (0.13 MB)

{kind=link}

답변 1

예스스탁 예스스탁 답변

2021-04-20 09:23:34

안녕하세요

예스스탁입니다.

1

해당 수식들 봉미완성에 발생하는 신호가 맞습니다.

첨부하신 그림에 보시면 매수손실 신호가 봉의 저가부근에서 발생한것을 확인하실수 있습니다.

신호가 발생한 봉의 옆에 조그만 세모표시가 신호가 발생한 위치입니다.

2

리포트의 신호의 날짜시간은 마우스로 봉 지정시 표시되는 날짜시간으로

신호가 발생한 봉이 대표날짜와 시간입니다.

신호가 발생한 가격의 날짜와 시간은 아닙니다.

3

리포트의 손익은 설정창 수수료와 슬리피지 설정이 적용됩니다.

해당 값을 0으로 하시면 손실이 160으로 표시되게 됩니다

즐거운 하루되세요

> 승부사1 님이 쓴 글입니다.

> 제목 : 볼린저 밴드 수식 점검 문의드립니다.

> 아래의 수식을 시뮬레이션 해보았습니다.

당일누적손실틱수를 160틱으로 잡아보았습니다.

그런데 160틱에서 손절되는게 아니고 봉이 완성될때까지 기다렸다가 시그널이 발생되는거 같습니다.

명령어를 Atstop으로 해서 당연히 되는줄 알았는데 아닌거 같아서요 ~

160틱에서 stop되게 하려면 무엇을 바꿔야 하는지 좀 알려주시면 감사하겠습니다.

- 아 래 -

Inputs: Length(9), StdDev(2), Bars(2);

Variables: BBTop(0),BBBot(0);

Input : 당일누적수익틱수(500),당일누적손실틱수(160);

input : starttime(100000),endtime(200000);

VARS: Tcond(false),N1(0),dayPl(0),당일누적수익(0),당일누적손실(0),Xcond(false),stok(0),stod(0);

if (sdate != sdate[1] and stime >= endtime) or

(sdate == sdate[1] and stime >= endtime and stime[1] < endtime) then

{

Tcond = false;

if MarketPosition == 1 Then

ExitLong("매수청산");

if MarketPosition == -1 Then

ExitShort("매도청산");

}

if (sdate != sdate[1] and stime >= starttime) or

(sdate == sdate[1] and stime >= starttime and stime[1] < starttime) then

{

Xcond = false;

N1 = NetProfit;

Tcond = true;

}

당일누적수익 = PriceScale*당일누적수익틱수;

당일누적손실 = PriceScale*당일누적손실틱수;

daypl = NetProfit-N1;

if TotalTrades > TotalTrades[1] then

{

if daypl >= 당일누적수익 or daypl <= -당일누적손실 Then

Xcond = true;

if (IsExitName("dbp",1) == true or IsExitName("dbl",1) == true or

IsExitName("dsp",1) == true or IsExitName("dsl",1) == true) then

Xcond = true;

}

if MarketPosition == 1 then{

ExitLong("매수수익",atlimit,EntryPrice+((당일누적수익-daypl)/CurrentContracts));

ExitLong("매수손실",AtStop,EntryPrice-((당일누적손실+daypl)/CurrentContracts));

}

if MarketPosition == -1 then{

ExitShort("매도수익",atlimit,EntryPrice-((당일누적수익-daypl)/CurrentContracts));

ExitShort("매도손실",AtStop,EntryPrice+((당일누적손실+daypl)/CurrentContracts));

}

BBTop = BollBandup(Length, StdDev);

BBBot = BollBanddown(Length, StdDev);

If Tcond == true and Xcond == False and CountIF(Close < BBBot, Bars) == Bars Then

Buy("매수", AtStop, BBBot);

If Tcond == true and Xcond == False and CountIF(Close > BBTop, Bars) == Bars Then

Sell("매도", AtStop, BBTop);

이전글