커뮤니티

추가 청산 로직 좀 부탁 드립니다.

2021-05-26 20:40:25

1093

글번호 149354

첨부 이미지

그림1

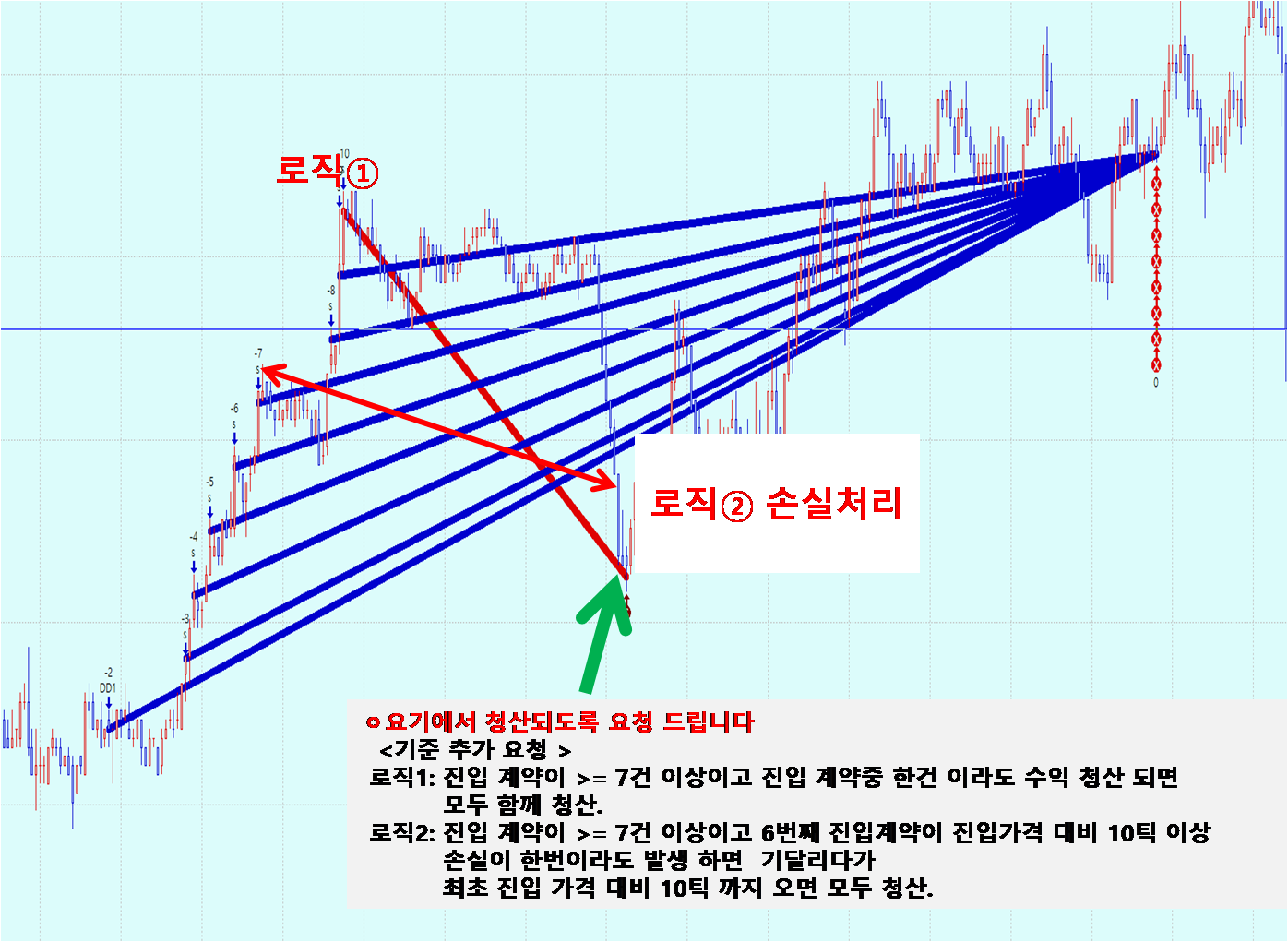

* 전일 수식중 추가 청산 로직이 생겨 부탁 좀 드립니다.

*로직1:진입 계약이 >= 7건 이상이고 건수중 한건 이라도 수익 청산 되면 모두 청산

*로직2:진입 계약이 >= 7건 이상이고 6번째 진입계약이 진입가격 대비 10틱 이상 손실이

한번이라도 발생 하면 기달리다가 최초 진입 가격 대비 10틱 까지 오면 모두 청산.

(적당한 가격에서 손실 청산)

## 수식

if MarketPosition == 1 Then

{

ExitLong("bx",AtLimit,EntryPrice+PriceScale*8);

if MaxContracts < 10 Then

Buy("b",AtLimit,LatestEntryPrice(0)-PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitLong("bx1",AtLimit,AvgEntryPrice+PriceScale*XX);

ExitLong("bx2",AtLimit,EntryPrice);

}

## 추가 로직1 : 7건 이상이고 진입 건수중 한계약 이라도 수익 청산 되면 모두 청산

## 추가 로직2 : 7건 이상이고 6번째 진입계약이 진입가격 대비 10틱 이상 손실이

한번이라도 발생 하면 기달리다가

최초 진입 가격 대비 10틱 까지 오면 모두 청산.

}

if MarketPosition == -1 Then

{

ExitShort("sx",AtLimit,EntryPrice-PriceScale*8);

if MaxContracts < 10 Then

Sell("s",AtLimit,LatestEntryPrice(0)+PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitShort("sx1",AtLimit,AvgEntryPrice-PriceScale*XX);

ExitShort("sx2",AtLimit,EntryPrice);

}

## 추가 로직1 : 7건 이상이고 진입 건수중 한계약 이라도 수익 청산 되면 모두 청산

## 추가 로직2 : 7건 이상이고 6번째 진입계약이 진입가격 대비 10틱 이상 손실이

한번이라도 발생 하면 기달리다가

최초 진입 가격 대비 10틱 까지 오면 모두 청산.

}

## 청산식

SetStopProfittarget(PriceScale*50,PointStop) ;

SetStopLoss(PriceScale*100,PointStop);

* 고맙습니다. 많은 도움에 감사 드립니다.

- 1. 매매식0526.png (0.32 MB)

{kind=link}

답변 3

예스스탁 예스스탁 답변

2021-05-27 13:29:41

안녕하세요

예스스탁입니다.

## 수식

if MarketPosition == 1 Then

{

ExitLong("bx",AtLimit,EntryPrice+PriceScale*8);

if MaxContracts < 10 Then

Buy("b",AtLimit,LatestEntryPrice(0)-PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitLong("bx1",AtLimit,AvgEntryPrice+PriceScale*XX);

ExitLong("bx2",AtLimit,EntryPrice);

}

if MaxEntries == 6 Then

Value1 = LatestEntryPrice(0);

if MaxEntries >= 6 Then

{

if L <= value1-PriceScale*10 Then

Condition1 = true;

}

if MaxEntries >= 7 and IsExitName("StopProfitTarget",1) == true Then

{

ExitLong("bx3");

}

if MaxEntries >= 7 and Condition1 == true Then

{

ExitLong("bx4",AtLimit,EntryPrice-PriceScale*10);

}

}

Else

Condition1 = False;

if MarketPosition == -1 Then

{

ExitShort("sx",AtLimit,EntryPrice-PriceScale*8);

if MaxContracts < 10 Then

Sell("s",AtLimit,LatestEntryPrice(0)+PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitShort("sx1",AtLimit,AvgEntryPrice-PriceScale*XX);

ExitShort("sx2",AtLimit,EntryPrice);

}

if MaxEntries == 6 Then

Value2 = LatestEntryPrice(0);

if MaxEntries >= 6 Then

{

if H >= value2+PriceScale*10 Then

Condition2 = true;

}

if MaxEntries >= 7 and IsExitName("StopProfitTarget",1) == true Then

{

ExitShort("sx3");

}

if MaxEntries >= 7 and Condition2 == true Then

{

ExitShort("sx4",AtLimit,EntryPrice+PriceScale*10);

}

}

Else

Condition2 = False;

## 청산식

SetStopProfittarget(PriceScale*50,PointStop) ;

SetStopLoss(PriceScale*100,PointStop);

즐거운 하루되세요

> 요타 님이 쓴 글입니다.

> 제목 : 추가 청산 로직 좀 부탁 드립니다.

> * 전일 수식중 추가 청산 로직이 생겨 부탁 좀 드립니다.

*로직1:진입 계약이 >= 7건 이상이고 건수중 한건 이라도 수익 청산 되면 모두 청산

*로직2:진입 계약이 >= 7건 이상이고 6번째 진입계약이 진입가격 대비 10틱 이상 손실이

한번이라도 발생 하면 기달리다가 최초 진입 가격 대비 10틱 까지 오면 모두 청산.

(적당한 가격에서 손실 청산)

## 수식

if MarketPosition == 1 Then

{

ExitLong("bx",AtLimit,EntryPrice+PriceScale*8);

if MaxContracts < 10 Then

Buy("b",AtLimit,LatestEntryPrice(0)-PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitLong("bx1",AtLimit,AvgEntryPrice+PriceScale*XX);

ExitLong("bx2",AtLimit,EntryPrice);

}

## 추가 로직1 : 7건 이상이고 진입 건수중 한계약 이라도 수익 청산 되면 모두 청산

## 추가 로직2 : 7건 이상이고 6번째 진입계약이 진입가격 대비 10틱 이상 손실이

한번이라도 발생 하면 기달리다가

최초 진입 가격 대비 10틱 까지 오면 모두 청산.

}

if MarketPosition == -1 Then

{

ExitShort("sx",AtLimit,EntryPrice-PriceScale*8);

if MaxContracts < 10 Then

Sell("s",AtLimit,LatestEntryPrice(0)+PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitShort("sx1",AtLimit,AvgEntryPrice-PriceScale*XX);

ExitShort("sx2",AtLimit,EntryPrice);

}

## 추가 로직1 : 7건 이상이고 진입 건수중 한계약 이라도 수익 청산 되면 모두 청산

## 추가 로직2 : 7건 이상이고 6번째 진입계약이 진입가격 대비 10틱 이상 손실이

한번이라도 발생 하면 기달리다가

최초 진입 가격 대비 10틱 까지 오면 모두 청산.

}

## 청산식

SetStopProfittarget(PriceScale*50,PointStop) ;

SetStopLoss(PriceScale*100,PointStop);

* 고맙습니다. 많은 도움에 감사 드립니다.

요타

2021-05-27 14:56:29

input : 시스템적용일(20210424), 시스템시작시간(080000),시스템종료시간(210000);

input : ntime(30),P1(20),P2(70),XX(20);

var : cnt(0),Xcnt(0),Ecnt(0),Tcond(False) ;

var : S1(0),D1(0),TM(0),TF(0);

var : sum1(0),mav1(0),sum2(0),mav2(0);

Array : CC[100](0);

if Bdate != Bdate[1] Then

{

S1 = TimeToMinutes(stime);

D1 = sdate;

}

if D1 > 0 then

{

if sdate == D1 Then

TM = TimeToMinutes(stime)-S1;

Else

TM = TimeToMinutes(stime)+1440-S1;

TF = TM%ntime;

if Bdate != Bdate[1] or

(Bdate == Bdate[1] and ntime > 1 and TF < TF[1]) or

(Bdate == Bdate[1] and ntime > 1 and TM >= TM[1]+ntime) or

(Bdate == Bdate[1] and ntime == 1 and TM > TM[1]) Then

{

for cnt = 1 to 99

{

CC[cnt] = CC[cnt-1][1];

}

}

CC[0] = C;

if CC[P1-1] > 0 then

{

sum1 = 0;

for cnt = 0 to P1-1

{

sum1 = sum1+CC[cnt];

}

mav1 = sum1/P1;

}

if CC[P2-1] > 0 then

{

sum2 = 0;

for cnt = 0 to P2-1

{

sum2 = sum2+CC[cnt];

}

mav2 = sum2/P2;

}

}

if 시스템종료시간 > 시스템시작시간 then

SetStopEndofday(시스템종료시간);

Else

{

if sDate != sDate[1] Then

SetStopEndofday(시스템종료시간);

}

if (sDate != sDate[1] and sTime >= 시스템종료시간) or (sDate == sDate[1] and sTime >= 시스템종료시간 and sTime[1] < 시스템종료시간) then

{

Tcond = False;

}

if (sDate != sDate[1] and sTime >= 시스템시작시간) or (sDate == sDate[1] and sTime >= 시스템시작시간 and sTime[1] < 시스템시작시간) then

{

Tcond = true;

Ecnt = 0;

Xcnt = 0 ;

if 시스템종료시간 < 시스템시작시간 then SetStopEndofday(0);

}

if (MarketPosition != 0 and MarketPosition != MarketPosition[1]) or (MarketPosition == MarketPosition[1] and TotalTrades > TotalTrades[1]) Then

Ecnt = Ecnt + 1;

if sdate >= 시스템적용일 and Tcond == true Then

{

## 매매식 입력

If stime < 080300 and mav1 > mav2 and mav1 > 0 and mav2 > 0 Then Buy("SS1",OnClose,DEF,2);

If stime < 080300 and mav1 < mav2 and mav1 > 0 and mav2 > 0 Then Sell("DD1",OnClose,DEF,2);

}

## 추가 매수식

## 수식

if MarketPosition == 1 Then

{

ExitLong("bx",AtLimit,EntryPrice+PriceScale*8);

if MaxContracts < 10 Then

Buy("b",AtLimit,LatestEntryPrice(0)-PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitLong("bx1",AtLimit,AvgEntryPrice+PriceScale*XX);

ExitLong("bx2",AtLimit,EntryPrice);

}

if MaxEntries == 6 Then

Value1 = LatestEntryPrice(0);

if MaxEntries >= 6 Then

{

if L <= value1-PriceScale*10 Then

Condition1 = true;

}

if MaxEntries >= 7 and IsExitName("StopProfitTarget",1) == true Then

{

ExitLong("bx3");

}

if MaxEntries >= 7 and Condition1 == true Then

{

ExitLong("bx4",AtLimit,EntryPrice-PriceScale*10);

}

}

Else

Condition1 = False;

if MarketPosition == -1 Then

{

ExitShort("sx",AtLimit,EntryPrice-PriceScale*8);

if MaxContracts < 10 Then

Sell("s",AtLimit,LatestEntryPrice(0)+PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitShort("sx1",AtLimit,AvgEntryPrice-PriceScale*XX);

ExitShort("sx2",AtLimit,EntryPrice);

}

if MaxEntries == 6 Then

Value2 = LatestEntryPrice(0);

if MaxEntries >= 6 Then

{

if H >= value2+PriceScale*10 Then

Condition2 = true;

}

if MaxEntries >= 7 and IsExitName("StopProfitTarget",1) == true Then

{

ExitShort("sx3");

}

if MaxEntries >= 7 and Condition2 == true Then

{

ExitShort("sx4",AtLimit,EntryPrice+PriceScale*10);

}

}

Else

Condition2 = False;

/* if MarketPosition == 1 Then

{

ExitLong("bx",AtLimit,EntryPrice+PriceScale*xx);

if MaxContracts < 10 Then

Buy("b",AtLimit,LatestEntryPrice(0)-PriceScale*10,1);

if MaxContracts >= 4 Then

ExitLong("bx1",AtLimit,AvgEntryPrice+PriceScale*XX);

}

if MarketPosition == -1 Then

{

ExitShort("sx",AtLimit,EntryPrice-PriceScale*xx);

if MaxContracts < 10 Then

Sell("s",AtLimit,LatestEntryPrice(0)+PriceScale*10,1);

if MaxContracts >= 2 Then

ExitShort("sx1",AtLimit,AvgEntryPrice-PriceScale*XX);*/

///}

## 청산식

SetStopProfittarget(PriceScale*40,PointStop) ;

SetStopLoss(PriceScale*80,PointStop);

> 예스스탁 님이 쓴 글입니다.

> 제목 : Re : 추가 청산 로직 좀 부탁 드립니다.

>

안녕하세요

예스스탁입니다.

## 수식

if MarketPosition == 1 Then

{

ExitLong("bx",AtLimit,EntryPrice+PriceScale*8);

if MaxContracts < 10 Then

Buy("b",AtLimit,LatestEntryPrice(0)-PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitLong("bx1",AtLimit,AvgEntryPrice+PriceScale*XX);

ExitLong("bx2",AtLimit,EntryPrice);

}

if MaxEntries == 6 Then

Value1 = LatestEntryPrice(0);

if MaxEntries >= 6 Then

{

if L <= value1-PriceScale*10 Then

Condition1 = true;

}

if MaxEntries >= 7 and IsExitName("StopProfitTarget",1) == true Then

{

ExitLong("bx3");

}

if MaxEntries >= 7 and Condition1 == true Then

{

ExitLong("bx4",AtLimit,EntryPrice-PriceScale*10);

}

}

Else

Condition1 = False;

if MarketPosition == -1 Then

{

ExitShort("sx",AtLimit,EntryPrice-PriceScale*8);

if MaxContracts < 10 Then

Sell("s",AtLimit,LatestEntryPrice(0)+PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitShort("sx1",AtLimit,AvgEntryPrice-PriceScale*XX);

ExitShort("sx2",AtLimit,EntryPrice);

}

if MaxEntries == 6 Then

Value2 = LatestEntryPrice(0);

if MaxEntries >= 6 Then

{

if H >= value2+PriceScale*10 Then

Condition2 = true;

}

if MaxEntries >= 7 and IsExitName("StopProfitTarget",1) == true Then

{

ExitShort("sx3");

}

if MaxEntries >= 7 and Condition2 == true Then

{

ExitShort("sx4",AtLimit,EntryPrice+PriceScale*10);

}

}

Else

Condition2 = False;

## 청산식

SetStopProfittarget(PriceScale*50,PointStop) ;

SetStopLoss(PriceScale*100,PointStop);

즐거운 하루되세요

> 요타 님이 쓴 글입니다.

> 제목 : 추가 청산 로직 좀 부탁 드립니다.

> * 전일 수식중 추가 청산 로직이 생겨 부탁 좀 드립니다.

*로직1:진입 계약이 >= 7건 이상이고 건수중 한건 이라도 수익 청산 되면 모두 청산

*로직2:진입 계약이 >= 7건 이상이고 6번째 진입계약이 진입가격 대비 10틱 이상 손실이

한번이라도 발생 하면 기달리다가 최초 진입 가격 대비 10틱 까지 오면 모두 청산.

(적당한 가격에서 손실 청산)

## 수식

if MarketPosition == 1 Then

{

ExitLong("bx",AtLimit,EntryPrice+PriceScale*8);

if MaxContracts < 10 Then

Buy("b",AtLimit,LatestEntryPrice(0)-PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitLong("bx1",AtLimit,AvgEntryPrice+PriceScale*XX);

ExitLong("bx2",AtLimit,EntryPrice);

}

## 추가 로직1 : 7건 이상이고 진입 건수중 한계약 이라도 수익 청산 되면 모두 청산

## 추가 로직2 : 7건 이상이고 6번째 진입계약이 진입가격 대비 10틱 이상 손실이

한번이라도 발생 하면 기달리다가

최초 진입 가격 대비 10틱 까지 오면 모두 청산.

}

if MarketPosition == -1 Then

{

ExitShort("sx",AtLimit,EntryPrice-PriceScale*8);

if MaxContracts < 10 Then

Sell("s",AtLimit,LatestEntryPrice(0)+PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitShort("sx1",AtLimit,AvgEntryPrice-PriceScale*XX);

ExitShort("sx2",AtLimit,EntryPrice);

}

## 추가 로직1 : 7건 이상이고 진입 건수중 한계약 이라도 수익 청산 되면 모두 청산

## 추가 로직2 : 7건 이상이고 6번째 진입계약이 진입가격 대비 10틱 이상 손실이

한번이라도 발생 하면 기달리다가

최초 진입 가격 대비 10틱 까지 오면 모두 청산.

}

## 청산식

SetStopProfittarget(PriceScale*50,PointStop) ;

SetStopLoss(PriceScale*100,PointStop);

* 고맙습니다. 많은 도움에 감사 드립니다.

예스스탁 예스스탁 답변

2021-05-27 15:10:58

안녕하세요

예스스탁입니다.

input : 시스템적용일(20210424), 시스템시작시간(080000),시스템종료시간(210000);

input : 익절틱수(40),손절틱수(20);

input : ntime(30),P1(20),P2(70),XX(20);

var : cnt(0),Xcnt(0),Ecnt(0),Tcond(False) ;

var : S1(0),D1(0),TM(0),TF(0);

var : sum1(0),mav1(0),sum2(0),mav2(0);

Array : CC[100](0);

if Bdate != Bdate[1] Then

{

S1 = TimeToMinutes(stime);

D1 = sdate;

}

if D1 > 0 then

{

if sdate == D1 Then

TM = TimeToMinutes(stime)-S1;

Else

TM = TimeToMinutes(stime)+1440-S1;

TF = TM%ntime;

if Bdate != Bdate[1] or

(Bdate == Bdate[1] and ntime > 1 and TF < TF[1]) or

(Bdate == Bdate[1] and ntime > 1 and TM >= TM[1]+ntime) or

(Bdate == Bdate[1] and ntime == 1 and TM > TM[1]) Then

{

for cnt = 1 to 99

{

CC[cnt] = CC[cnt-1][1];

}

}

CC[0] = C;

if CC[P1-1] > 0 then

{

sum1 = 0;

for cnt = 0 to P1-1

{

sum1 = sum1+CC[cnt];

}

mav1 = sum1/P1;

}

if CC[P2-1] > 0 then

{

sum2 = 0;

for cnt = 0 to P2-1

{

sum2 = sum2+CC[cnt];

}

mav2 = sum2/P2;

}

}

if 시스템종료시간 > 시스템시작시간 then

SetStopEndofday(시스템종료시간);

Else

{

if sDate != sDate[1] Then

SetStopEndofday(시스템종료시간);

}

if (sDate != sDate[1] and sTime >= 시스템종료시간) or (sDate == sDate[1] and sTime >= 시스템종료시간 and sTime[1] < 시스템종료시간) then

{

Tcond = False;

}

if (sDate != sDate[1] and sTime >= 시스템시작시간) or (sDate == sDate[1] and sTime >= 시스템시작시간 and sTime[1] < 시스템시작시간) then

{

Tcond = true;

Ecnt = 0;

Xcnt = 0 ;

if 시스템종료시간 < 시스템시작시간 then SetStopEndofday(0);

}

if (MarketPosition != 0 and MarketPosition != MarketPosition[1]) or (MarketPosition == MarketPosition[1] and TotalTrades > TotalTrades[1]) Then

Ecnt = Ecnt + 1;

if sdate >= 시스템적용일 and Tcond == true Then

{

## 매매식 입력

If stime < 080300 and mav1 > mav2 and mav1 > 0 and mav2 > 0 Then Buy("SS1",OnClose,DEF,2);

If stime < 080300 and mav1 < mav2 and mav1 > 0 and mav2 > 0 Then Sell("DD1",OnClose,DEF,2);

}

## 추가 매수식

## 수식

if MarketPosition == 1 Then

{

ExitLong("bx",AtLimit,EntryPrice+PriceScale*8);

if MaxContracts < 10 Then

Buy("b",AtLimit,LatestEntryPrice(0)-PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitLong("bx1",AtLimit,AvgEntryPrice+PriceScale*XX);

ExitLong("bx2",AtLimit,EntryPrice);

}

if MaxEntries == 6 Then

Value1 = LatestEntryPrice(0);

if MaxEntries >= 6 Then

{

if L <= value1-PriceScale*10 Then

Condition1 = true;

}

if MaxEntries >= 7 Then

{

ExitLong("bx3",AtLimit,LatestEntryPrice(0)+PriceScale*익절틱수);

}

if MaxEntries >= 7 and Condition1 == true Then

{

ExitLong("bx4",AtLimit,EntryPrice-PriceScale*10);

}

}

Else

Condition1 = False;

if MarketPosition == -1 Then

{

ExitShort("sx",AtLimit,EntryPrice-PriceScale*8);

if MaxContracts < 10 Then

Sell("s",AtLimit,LatestEntryPrice(0)+PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitShort("sx1",AtLimit,AvgEntryPrice-PriceScale*XX);

ExitShort("sx2",AtLimit,EntryPrice);

}

if MaxEntries == 6 Then

Value2 = LatestEntryPrice(0);

if MaxEntries >= 6 Then

{

if H >= value2+PriceScale*10 Then

Condition2 = true;

}

if MaxEntries >= 7 Then

{

ExitShort("sx3",AtLimit,LatestEntryPrice(0)-PriceScale*익절틱수);

}

if MaxEntries >= 7 and Condition2 == true Then

{

ExitShort("sx4",AtLimit,EntryPrice+PriceScale*10);

}

}

Else

Condition2 = False;

/* if MarketPosition == 1 Then

{

ExitLong("bx",AtLimit,EntryPrice+PriceScale*xx);

if MaxContracts < 10 Then

Buy("b",AtLimit,LatestEntryPrice(0)-PriceScale*10,1);

if MaxContracts >= 4 Then

ExitLong("bx1",AtLimit,AvgEntryPrice+PriceScale*XX);

}

if MarketPosition == -1 Then

{

ExitShort("sx",AtLimit,EntryPrice-PriceScale*xx);

if MaxContracts < 10 Then

Sell("s",AtLimit,LatestEntryPrice(0)+PriceScale*10,1);

if MaxContracts >= 2 Then

ExitShort("sx1",AtLimit,AvgEntryPrice-PriceScale*XX);*/

///}

## 청산식

SetStopProfittarget(PriceScale*익절틱수,PointStop) ;

SetStopLoss(PriceScale*손절틱수,PointStop);

즐거운 하루되세요

> 요타 님이 쓴 글입니다.

> 제목 : Re : Re : 추가 청산 로직 좀 부탁 드립니다.

>

input : 시스템적용일(20210424), 시스템시작시간(080000),시스템종료시간(210000);

input : ntime(30),P1(20),P2(70),XX(20);

var : cnt(0),Xcnt(0),Ecnt(0),Tcond(False) ;

var : S1(0),D1(0),TM(0),TF(0);

var : sum1(0),mav1(0),sum2(0),mav2(0);

Array : CC[100](0);

if Bdate != Bdate[1] Then

{

S1 = TimeToMinutes(stime);

D1 = sdate;

}

if D1 > 0 then

{

if sdate == D1 Then

TM = TimeToMinutes(stime)-S1;

Else

TM = TimeToMinutes(stime)+1440-S1;

TF = TM%ntime;

if Bdate != Bdate[1] or

(Bdate == Bdate[1] and ntime > 1 and TF < TF[1]) or

(Bdate == Bdate[1] and ntime > 1 and TM >= TM[1]+ntime) or

(Bdate == Bdate[1] and ntime == 1 and TM > TM[1]) Then

{

for cnt = 1 to 99

{

CC[cnt] = CC[cnt-1][1];

}

}

CC[0] = C;

if CC[P1-1] > 0 then

{

sum1 = 0;

for cnt = 0 to P1-1

{

sum1 = sum1+CC[cnt];

}

mav1 = sum1/P1;

}

if CC[P2-1] > 0 then

{

sum2 = 0;

for cnt = 0 to P2-1

{

sum2 = sum2+CC[cnt];

}

mav2 = sum2/P2;

}

}

if 시스템종료시간 > 시스템시작시간 then

SetStopEndofday(시스템종료시간);

Else

{

if sDate != sDate[1] Then

SetStopEndofday(시스템종료시간);

}

if (sDate != sDate[1] and sTime >= 시스템종료시간) or (sDate == sDate[1] and sTime >= 시스템종료시간 and sTime[1] < 시스템종료시간) then

{

Tcond = False;

}

if (sDate != sDate[1] and sTime >= 시스템시작시간) or (sDate == sDate[1] and sTime >= 시스템시작시간 and sTime[1] < 시스템시작시간) then

{

Tcond = true;

Ecnt = 0;

Xcnt = 0 ;

if 시스템종료시간 < 시스템시작시간 then SetStopEndofday(0);

}

if (MarketPosition != 0 and MarketPosition != MarketPosition[1]) or (MarketPosition == MarketPosition[1] and TotalTrades > TotalTrades[1]) Then

Ecnt = Ecnt + 1;

if sdate >= 시스템적용일 and Tcond == true Then

{

## 매매식 입력

If stime < 080300 and mav1 > mav2 and mav1 > 0 and mav2 > 0 Then Buy("SS1",OnClose,DEF,2);

If stime < 080300 and mav1 < mav2 and mav1 > 0 and mav2 > 0 Then Sell("DD1",OnClose,DEF,2);

}

## 추가 매수식

## 수식

if MarketPosition == 1 Then

{

ExitLong("bx",AtLimit,EntryPrice+PriceScale*8);

if MaxContracts < 10 Then

Buy("b",AtLimit,LatestEntryPrice(0)-PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitLong("bx1",AtLimit,AvgEntryPrice+PriceScale*XX);

ExitLong("bx2",AtLimit,EntryPrice);

}

if MaxEntries == 6 Then

Value1 = LatestEntryPrice(0);

if MaxEntries >= 6 Then

{

if L <= value1-PriceScale*10 Then

Condition1 = true;

}

if MaxEntries >= 7 and IsExitName("StopProfitTarget",1) == true Then

{

ExitLong("bx3");

}

if MaxEntries >= 7 and Condition1 == true Then

{

ExitLong("bx4",AtLimit,EntryPrice-PriceScale*10);

}

}

Else

Condition1 = False;

if MarketPosition == -1 Then

{

ExitShort("sx",AtLimit,EntryPrice-PriceScale*8);

if MaxContracts < 10 Then

Sell("s",AtLimit,LatestEntryPrice(0)+PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitShort("sx1",AtLimit,AvgEntryPrice-PriceScale*XX);

ExitShort("sx2",AtLimit,EntryPrice);

}

if MaxEntries == 6 Then

Value2 = LatestEntryPrice(0);

if MaxEntries >= 6 Then

{

if H >= value2+PriceScale*10 Then

Condition2 = true;

}

if MaxEntries >= 7 and IsExitName("StopProfitTarget",1) == true Then

{

ExitShort("sx3");

}

if MaxEntries >= 7 and Condition2 == true Then

{

ExitShort("sx4",AtLimit,EntryPrice+PriceScale*10);

}

}

Else

Condition2 = False;

/* if MarketPosition == 1 Then

{

ExitLong("bx",AtLimit,EntryPrice+PriceScale*xx);

if MaxContracts < 10 Then

Buy("b",AtLimit,LatestEntryPrice(0)-PriceScale*10,1);

if MaxContracts >= 4 Then

ExitLong("bx1",AtLimit,AvgEntryPrice+PriceScale*XX);

}

if MarketPosition == -1 Then

{

ExitShort("sx",AtLimit,EntryPrice-PriceScale*xx);

if MaxContracts < 10 Then

Sell("s",AtLimit,LatestEntryPrice(0)+PriceScale*10,1);

if MaxContracts >= 2 Then

ExitShort("sx1",AtLimit,AvgEntryPrice-PriceScale*XX);*/

///}

## 청산식

SetStopProfittarget(PriceScale*40,PointStop) ;

SetStopLoss(PriceScale*80,PointStop);

> 예스스탁 님이 쓴 글입니다.

> 제목 : Re : 추가 청산 로직 좀 부탁 드립니다.

>

안녕하세요

예스스탁입니다.

## 수식

if MarketPosition == 1 Then

{

ExitLong("bx",AtLimit,EntryPrice+PriceScale*8);

if MaxContracts < 10 Then

Buy("b",AtLimit,LatestEntryPrice(0)-PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitLong("bx1",AtLimit,AvgEntryPrice+PriceScale*XX);

ExitLong("bx2",AtLimit,EntryPrice);

}

if MaxEntries == 6 Then

Value1 = LatestEntryPrice(0);

if MaxEntries >= 6 Then

{

if L <= value1-PriceScale*10 Then

Condition1 = true;

}

if MaxEntries >= 7 and IsExitName("StopProfitTarget",1) == true Then

{

ExitLong("bx3");

}

if MaxEntries >= 7 and Condition1 == true Then

{

ExitLong("bx4",AtLimit,EntryPrice-PriceScale*10);

}

}

Else

Condition1 = False;

if MarketPosition == -1 Then

{

ExitShort("sx",AtLimit,EntryPrice-PriceScale*8);

if MaxContracts < 10 Then

Sell("s",AtLimit,LatestEntryPrice(0)+PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitShort("sx1",AtLimit,AvgEntryPrice-PriceScale*XX);

ExitShort("sx2",AtLimit,EntryPrice);

}

if MaxEntries == 6 Then

Value2 = LatestEntryPrice(0);

if MaxEntries >= 6 Then

{

if H >= value2+PriceScale*10 Then

Condition2 = true;

}

if MaxEntries >= 7 and IsExitName("StopProfitTarget",1) == true Then

{

ExitShort("sx3");

}

if MaxEntries >= 7 and Condition2 == true Then

{

ExitShort("sx4",AtLimit,EntryPrice+PriceScale*10);

}

}

Else

Condition2 = False;

## 청산식

SetStopProfittarget(PriceScale*50,PointStop) ;

SetStopLoss(PriceScale*100,PointStop);

즐거운 하루되세요

> 요타 님이 쓴 글입니다.

> 제목 : 추가 청산 로직 좀 부탁 드립니다.

> * 전일 수식중 추가 청산 로직이 생겨 부탁 좀 드립니다.

*로직1:진입 계약이 >= 7건 이상이고 건수중 한건 이라도 수익 청산 되면 모두 청산

*로직2:진입 계약이 >= 7건 이상이고 6번째 진입계약이 진입가격 대비 10틱 이상 손실이

한번이라도 발생 하면 기달리다가 최초 진입 가격 대비 10틱 까지 오면 모두 청산.

(적당한 가격에서 손실 청산)

## 수식

if MarketPosition == 1 Then

{

ExitLong("bx",AtLimit,EntryPrice+PriceScale*8);

if MaxContracts < 10 Then

Buy("b",AtLimit,LatestEntryPrice(0)-PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitLong("bx1",AtLimit,AvgEntryPrice+PriceScale*XX);

ExitLong("bx2",AtLimit,EntryPrice);

}

## 추가 로직1 : 7건 이상이고 진입 건수중 한계약 이라도 수익 청산 되면 모두 청산

## 추가 로직2 : 7건 이상이고 6번째 진입계약이 진입가격 대비 10틱 이상 손실이

한번이라도 발생 하면 기달리다가

최초 진입 가격 대비 10틱 까지 오면 모두 청산.

}

if MarketPosition == -1 Then

{

ExitShort("sx",AtLimit,EntryPrice-PriceScale*8);

if MaxContracts < 10 Then

Sell("s",AtLimit,LatestEntryPrice(0)+PriceScale*7,1);

if MaxContracts >= 4 and MaxContracts < 7 Then

{

ExitShort("sx1",AtLimit,AvgEntryPrice-PriceScale*XX);

ExitShort("sx2",AtLimit,EntryPrice);

}

## 추가 로직1 : 7건 이상이고 진입 건수중 한계약 이라도 수익 청산 되면 모두 청산

## 추가 로직2 : 7건 이상이고 6번째 진입계약이 진입가격 대비 10틱 이상 손실이

한번이라도 발생 하면 기달리다가

최초 진입 가격 대비 10틱 까지 오면 모두 청산.

}

## 청산식

SetStopProfittarget(PriceScale*50,PointStop) ;

SetStopLoss(PriceScale*100,PointStop);

* 고맙습니다. 많은 도움에 감사 드립니다.