커뮤니티

시스템식 문의 드립니다.

2021-08-03 22:32:21

988

글번호 151292

첨부 이미지

그림1

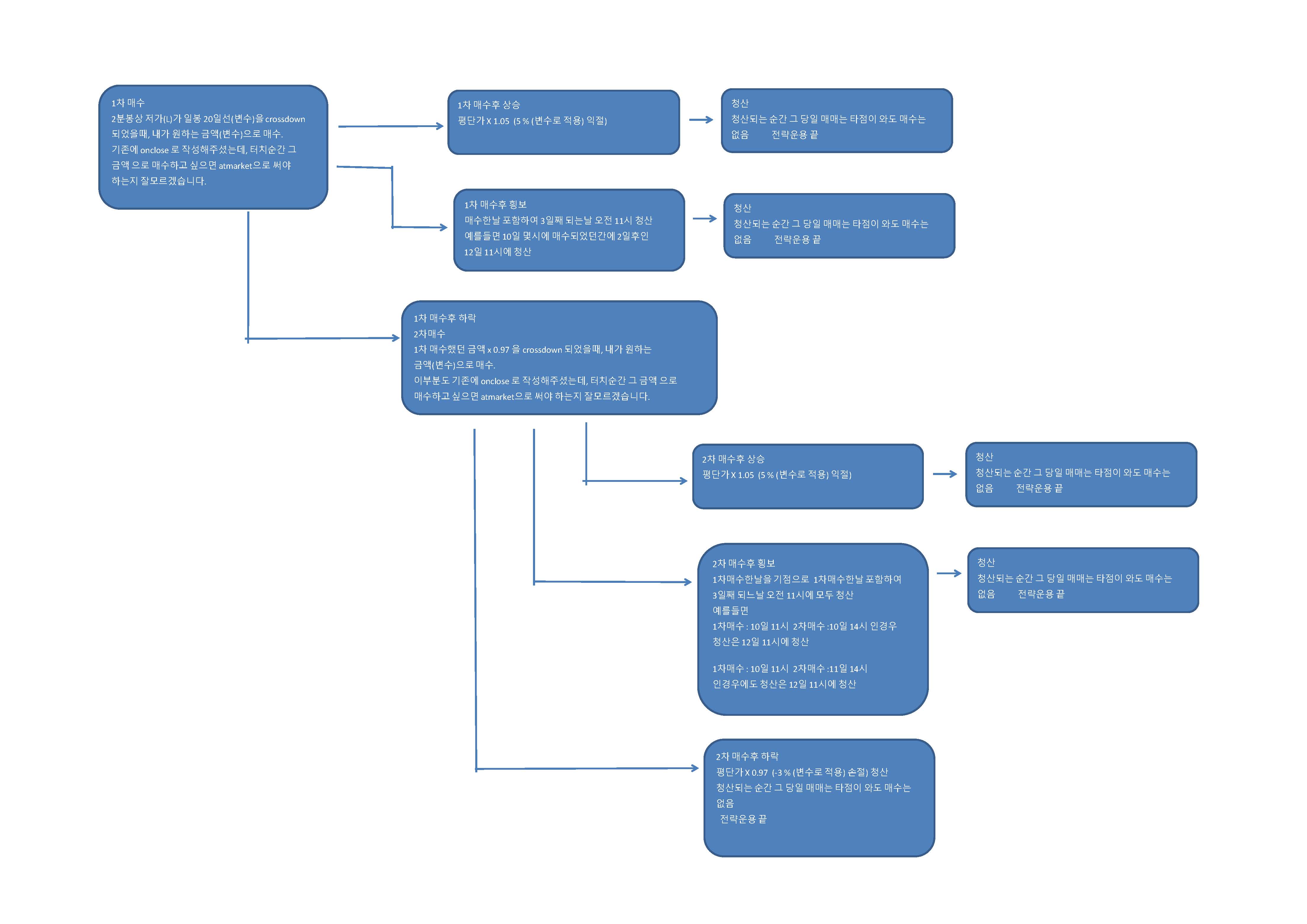

예전에 분봉에서 일봉상 이평선을 터치했을때 매수 하는

시스템식을 도식화해서 요청드린 사람입니다

벌써 똑같은 식으로 3번이나 질문하네요..

죄송합니다...ㅜ.ㅜ

이정도 실력도 없는 제 자신이 한심스럽네요..ㅜ.ㅜ

기존식에서 추가되는 조건이 생겨서 이리저리

수정을 해봤는데..잘안되어서 또 요청드리게 되었습니다.

새로 추가되는 조건은

1차 매수를 했던, 2차 매수까지 진행되었던건 간에

매수한지 2일차 13:00 가 되면.. 익절 퍼센트를 2% (변수 익절3) 로 수정되는식으로

조건을 추가하고 싶습니다.

예) 8/3일에 1차매수.. 8/3일 2차매수 ==> 익절타점5%가 안오고 횡보하는경우

8/4일 13:00 이후에 익절타점이 2%으로 변경

8/3일에 1차매수.. 8/4일 2차매수 ==> 익절타점5%가 안오고 횡보하는경우

8/4일 13:00 이후에 익절타점이 2%으로 변경

8/3일에 1차매수.. ==> 익절타점5%가 안오고 횡보하는경우

8/4일 13:00 이후에 익절타점이 2%으로 변경

xdate 와 xtime으로 만들어볼려고 이리지리 해봤는데.. 잘안됩니다..ㅜ.ㅜ

매번 감사하고 죄송하네요

요청드렸던 식 다시 올려드립니다.

------------------------------------------------------------------------

input : N(10),금액1(10000000),금액2(10000000);

input : 추가진입(-3),익절1(5),익절2(5),손절(-3);

input : Xdate(3),Xtime(110000);

var : cnt(0),sum(0),mav(0),DD(0);

sum = 0;

For cnt = 0 to N-1

{

sum = sum + DayClose(cnt);

}

mav = sum/N;

if Bdate != Bdate[1] Then

{

DD = DD+1;

Condition1 = False;

}

if MarketPosition == 0 and TotalTrades > TotalTrades[1] Then

Condition1 = true;

if Condition1 == False and MarketPosition == 0 and L > mav Then

Buy("b1",AtLimit,mav,Floor(금액1/min(NextBarOpen,mav)));

if MarketPosition == 1 Then

{

if DD == DD[BarsSinceEntry]+Xdate and sTime == xtime Then

{

Condition1 = true;

ExitLong("bx");

}

if MaxEntries == 1 and Condition1 == False Then

{

Buy("b2",AtLimit,LatestEntryPrice(0)*(1+추가진입/100),Floor(금액2/min(NextBarOpen,LatestEntryPrice(0)*(1+추가진입/100))));

ExitLong("Bp1",AtLimit,avgEntryPrice*(1+익절1/100));

}

if MaxEntries == 2 Then

{

ExitLong("Bp2",AtLimit,avgEntryPrice*(1+익절2/100));

ExitLong("Bl",AtStop,avgEntryPrice*(1+손절/100));

}

}

- 1. 152021_도식화.jpg (0.40 MB)

{kind=link}

답변 1

예스스탁 예스스탁 답변

2021-08-04 10:03:53

안녕하세요

예스스탁입니다.

input : N(10),금액1(10000000),금액2(10000000);

input : 추가진입(-3),익절1(5),익절2(5),익절3(3),손절(-3);

input : Xdate1(3),Xtime1(110000);

input : Xdate2(2),Xtime2(130000);

var : cnt(0),sum(0),mav(0),DD(0);

sum = 0;

For cnt = 0 to N-1

{

sum = sum + DayClose(cnt);

}

mav = sum/N;

if Bdate != Bdate[1] Then

{

DD = DD+1;

Condition1 = False;

}

if MarketPosition == 0 and TotalTrades > TotalTrades[1] Then

Condition1 = true;

if Condition1 == False and MarketPosition == 0 and L > mav Then

Buy("b1",AtLimit,mav,Floor(금액1/min(NextBarOpen,mav)));

if MarketPosition == 1 Then

{

if DD == DD[BarsSinceEntry]+Xdate1 and sTime == xtime1 Then

{

Condition1 = true;

ExitLong("bx");

}

#2일차 13시가 되면 condition1변수는 true로 변경

if DD == DD[BarsSinceEntry]+Xdate2 and sTime >= xtime2 Then

Condition2 = true;

if MaxEntries == 1 and Condition1 == False Then

{

Buy("b2",AtLimit,LatestEntryPrice(0)*(1+추가진입/100),Floor(금액2/min(NextBarOpen,LatestEntryPrice(0)*(1+추가진입/100))));

#Condition2가 False 일때만

if Condition2 == False Then

ExitLong("Bp1",AtLimit,avgEntryPrice*(1+익절1/100));

}

if MaxEntries == 2 Then

{

ExitLong("Bl",AtStop,avgEntryPrice*(1+손절/100));

#Condition2가 False 일때만

if Condition2 == False Then

ExitLong("Bp2",AtLimit,avgEntryPrice*(1+익절2/100));

}

#condition2변수가 true가 되면 익절3으로 감시

if Condition2 == true Then

ExitLong("Bp3",AtLimit,avgEntryPrice*(1+익절3/100));

}

Else

Condition2 = False;#매수전에는 condition2변수는 false

즐거운 하루되세요

> 맴맴잉 님이 쓴 글입니다.

> 제목 : 시스템식 문의 드립니다.

> 예전에 분봉에서 일봉상 이평선을 터치했을때 매수 하는

시스템식을 도식화해서 요청드린 사람입니다

벌써 똑같은 식으로 3번이나 질문하네요..

죄송합니다...ㅜ.ㅜ

이정도 실력도 없는 제 자신이 한심스럽네요..ㅜ.ㅜ

기존식에서 추가되는 조건이 생겨서 이리저리

수정을 해봤는데..잘안되어서 또 요청드리게 되었습니다.

새로 추가되는 조건은

1차 매수를 했던, 2차 매수까지 진행되었던건 간에

매수한지 2일차 13:00 가 되면.. 익절 퍼센트를 2% (변수 익절3) 로 수정되는식으로

조건을 추가하고 싶습니다.

예) 8/3일에 1차매수.. 8/3일 2차매수 ==> 익절타점5%가 안오고 횡보하는경우

8/4일 13:00 이후에 익절타점이 2%으로 변경

8/3일에 1차매수.. 8/4일 2차매수 ==> 익절타점5%가 안오고 횡보하는경우

8/4일 13:00 이후에 익절타점이 2%으로 변경

8/3일에 1차매수.. ==> 익절타점5%가 안오고 횡보하는경우

8/4일 13:00 이후에 익절타점이 2%으로 변경

xdate 와 xtime으로 만들어볼려고 이리지리 해봤는데.. 잘안됩니다..ㅜ.ㅜ

매번 감사하고 죄송하네요

요청드렸던 식 다시 올려드립니다.

------------------------------------------------------------------------

input : N(10),금액1(10000000),금액2(10000000);

input : 추가진입(-3),익절1(5),익절2(5),손절(-3);

input : Xdate(3),Xtime(110000);

var : cnt(0),sum(0),mav(0),DD(0);

sum = 0;

For cnt = 0 to N-1

{

sum = sum + DayClose(cnt);

}

mav = sum/N;

if Bdate != Bdate[1] Then

{

DD = DD+1;

Condition1 = False;

}

if MarketPosition == 0 and TotalTrades > TotalTrades[1] Then

Condition1 = true;

if Condition1 == False and MarketPosition == 0 and L > mav Then

Buy("b1",AtLimit,mav,Floor(금액1/min(NextBarOpen,mav)));

if MarketPosition == 1 Then

{

if DD == DD[BarsSinceEntry]+Xdate and sTime == xtime Then

{

Condition1 = true;

ExitLong("bx");

}

if MaxEntries == 1 and Condition1 == False Then

{

Buy("b2",AtLimit,LatestEntryPrice(0)*(1+추가진입/100),Floor(금액2/min(NextBarOpen,LatestEntryPrice(0)*(1+추가진입/100))));

ExitLong("Bp1",AtLimit,avgEntryPrice*(1+익절1/100));

}

if MaxEntries == 2 Then

{

ExitLong("Bp2",AtLimit,avgEntryPrice*(1+익절2/100));

ExitLong("Bl",AtStop,avgEntryPrice*(1+손절/100));

}

}

다음글