커뮤니티

수식 부탁드립니다

2021-11-04 06:57:18

837

글번호 153337

첨부 이미지

그림1

input : StartTime(233000),EndTime(030000);

var : 전환선(0),기준선(0),선행스팬1(0),선행스팬2(0);

var : Tcond(false);

if sDate != sDate[1] then

SetStopEndofday(Endtime);

if (sdate != sdate[1] and stime >= EndTime) or

(sdate == sdate[1] and stime >= EndTime and stime[1] < EndTime) Then

Tcond = False;

if (sdate != sdate[1] and stime >= StartTime) or

(sdate == sdate[1] and stime >= StartTime and stime[1] < StartTime) Then

{

Tcond = true;

SetStopEndofday(0);

}

var : entry(0);

if bdate != bdate[1] Then

entry = 0;

if (MarketPosition != 0 and MarketPosition != MarketPosition[1]) or

(MarketPosition == MarketPosition[1] and TotalTrades > TotalTrades[1]) Then

entry = entry+1;

if MarketPosition <= 0 and entry < 1 Then

buy("b",atlimit,dayhigh-PriceScale*20);

if MarketPosition == 1 Then

exitlong("bx",atlimit,lowest(L,BarsSinceEntry)+PriceScale*20);

if MarketPosition >= 0 and entry < 1 Then

sell("s",atlimit,daylow+PriceScale*30);

if MarketPosition == -1 Then

ExitShort("sx",atlimit,Highest(H,BarsSinceEntry)-PriceScale*30);

---------------------------

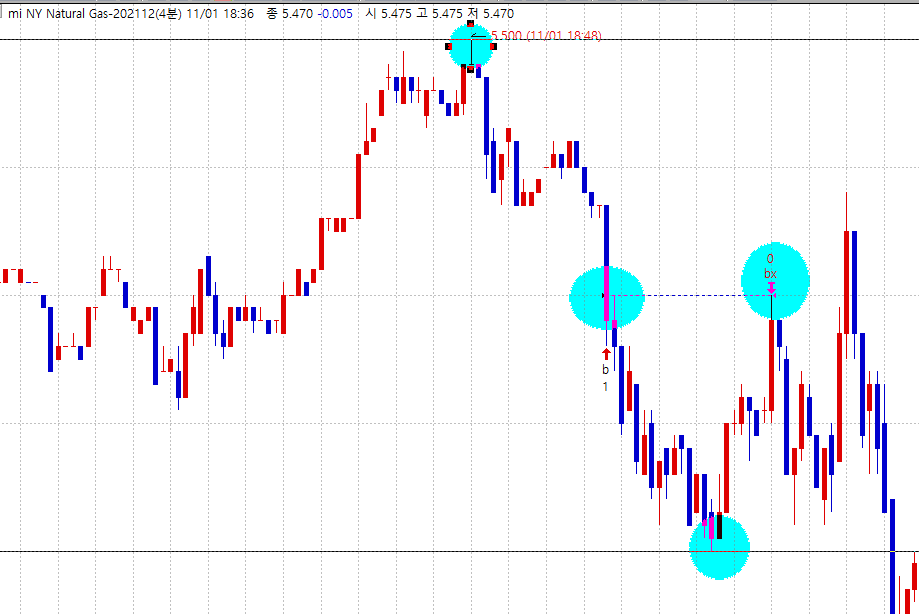

위 시스템의 매매신호는 당일 고저가대비 매수,매도의 청산 수식 입니다.

수정할것은 당일 고저가대비 매수,매도의 신호에서 청산은 그 진입신호에서

틱폭의 숫자만큼 청산이 되도록 부탁드립니다

늘 감사합니다

- 1. 로직.png (0.03 MB)

{kind=link}

답변 1

예스스탁 예스스탁 답변

2021-11-04 11:36:41

안녕하세요

예스스탁입니다.

input : StartTime(233000),EndTime(030000);

var : 전환선(0),기준선(0),선행스팬1(0),선행스팬2(0);

var : Tcond(false);

if sDate != sDate[1] then

SetStopEndofday(Endtime);

if (sdate != sdate[1] and stime >= EndTime) or

(sdate == sdate[1] and stime >= EndTime and stime[1] < EndTime) Then

Tcond = False;

if (sdate != sdate[1] and stime >= StartTime) or

(sdate == sdate[1] and stime >= StartTime and stime[1] < StartTime) Then

{

Tcond = true;

SetStopEndofday(0);

}

var : entry(0);

if bdate != bdate[1] Then

entry = 0;

if (MarketPosition != 0 and MarketPosition != MarketPosition[1]) or

(MarketPosition == MarketPosition[1] and TotalTrades > TotalTrades[1]) Then

entry = entry+1;

if MarketPosition <= 0 and entry < 1 Then

buy("b",atlimit,dayhigh-PriceScale*20);

if MarketPosition == 1 Then

exitlong("bx",atlimit,EntryPrice+PriceScale*20);

if MarketPosition >= 0 and entry < 1 Then

sell("s",atlimit,daylow+PriceScale*30);

if MarketPosition == -1 Then

ExitShort("sx",atlimit,EntryPrice-PriceScale*30);

즐거운 하루되세요

> 푸른 님이 쓴 글입니다.

> 제목 : 수식 부탁드립니다

> input : StartTime(233000),EndTime(030000);

var : 전환선(0),기준선(0),선행스팬1(0),선행스팬2(0);

var : Tcond(false);

if sDate != sDate[1] then

SetStopEndofday(Endtime);

if (sdate != sdate[1] and stime >= EndTime) or

(sdate == sdate[1] and stime >= EndTime and stime[1] < EndTime) Then

Tcond = False;

if (sdate != sdate[1] and stime >= StartTime) or

(sdate == sdate[1] and stime >= StartTime and stime[1] < StartTime) Then

{

Tcond = true;

SetStopEndofday(0);

}

var : entry(0);

if bdate != bdate[1] Then

entry = 0;

if (MarketPosition != 0 and MarketPosition != MarketPosition[1]) or

(MarketPosition == MarketPosition[1] and TotalTrades > TotalTrades[1]) Then

entry = entry+1;

if MarketPosition <= 0 and entry < 1 Then

buy("b",atlimit,dayhigh-PriceScale*20);

if MarketPosition == 1 Then

exitlong("bx",atlimit,lowest(L,BarsSinceEntry)+PriceScale*20);

if MarketPosition >= 0 and entry < 1 Then

sell("s",atlimit,daylow+PriceScale*30);

if MarketPosition == -1 Then

ExitShort("sx",atlimit,Highest(H,BarsSinceEntry)-PriceScale*30);

---------------------------

위 시스템의 매매신호는 당일 고저가대비 매수,매도의 청산 수식 입니다.

수정할것은 당일 고저가대비 매수,매도의 신호에서 청산은 그 진입신호에서

틱폭의 숫자만큼 청산이 되도록 부탁드립니다

늘 감사합니다