커뮤니티

CT를 YT로 변환

2022-04-12 09:25:41

1680

글번호 157942

첨부 이미지

그림1

수고하십니다.

공부목적으로 대신 CT 수식을 예트로 처음 변환하여 보았습니다.

pdf 파일인지라 복사붙이기가 깨끗하게 안나오는군요

무엇이 잘못되었는지 ,

변환된 예트 시스템식이 CT식과는 진입/청산이 틀리게 작동을 합니다

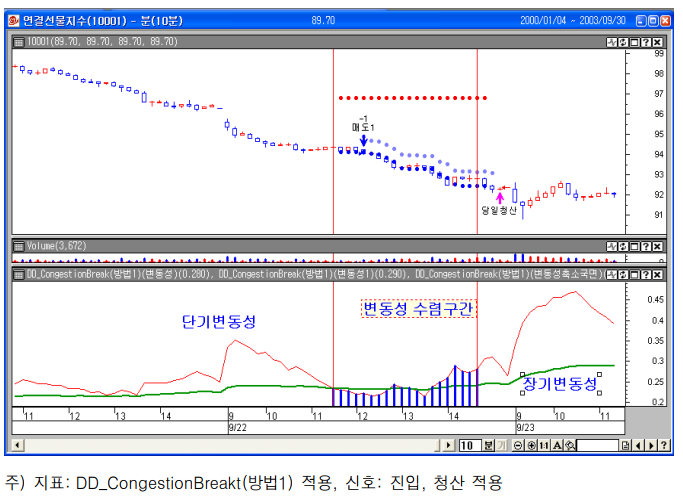

var1, var2를 장단기지표로 보고, CT지표로 나온 그림과 비교하였는데,

차트 세팅을 잘못한것인지(수정주가 on|off 둘 다 해봄) 차이가 좀 많이 나네요??!!!

아마도 CT함수와 YT함수 매칭이 잘못된 것 같은데, 체크 부탁 드립니다.

수정하신 부분에 기존소스 주석처리와 함께 설명도 부탁드리겠습니다.

그리고, 매수|매도와 매수1|매도1의 차이가 무엇인지요?

시간이 되면 원격접속 부탁 드리겠습니다.

#======================================================#

# CT <수식 0-11> DD_CongestionBreak(방법1)

#======================================================#

Input: len(10), len1(70), len2(0.37), s1(2.7), method(1), delay(8)

If method=1 Then

Var1=atr(len)

Var2=atr(len1)

Elseif method=2 Then

Var20=high-low

Var1=mov(Var20,len,s)

Var2=mov(Var20,len1,s)

End If

Cond1=tdate=exitdate(1) And position(1)=1

Cond2=tdate=exitdate(1) And position(1)=-1

If Var1<var2 Then

Var10=1

Else

Var10=0

EndIf

If hhv(1,Var10,delay)=1 Then

If ttime<1500 Then

If Cond1=False And high<opend+(highd(1)-lowd(1))*len2 Then

Call buy("매수",Atstop,Def,opend+(highd(1)-lowd(1))*len2)

End If

IfCond2=False And low>opend-(highd(1)-lowd(1))*len2 Then

Call sell("매도",Atstop,Def,opend-(highd(1)-lowd(1))*len2)

End If

If Cond1=False And high>opend+(highd(1)-lowd(1))*len2 Then

Call buy("매수1",Atstop,Def,hhv(1,high,delay))

End If

If Cond2=False And low<opend-(highd(1)-lowd(1))*len2 Then

Callsell("매도1",Atstop,Def,llv(1,low,delay))

End If

End if

End If

If position<>0then

Call exitlong("매수청산",Atstop,hhv(1,high,barnumsinceentry+1)-atr(20)*s1)

Call exitshort("매도청산",Atstop,llv(1,low,barnumsinceentry+1)+atr(20)*s1)

EndIf

#======================================================#

# YT <수식 0-11> DD_CongestionBreak(방법1)

#======================================================#

Input: len(10), len1(70), len2(0.37), s1(2.7), method(1), delay(8);

If method == 1 Then {

Var1=atr(len);

Var2=atr(len1) ;

}

Else if method == 2 Then {

Var20 = high - low;

Var1 = ma(Var20,len);

Var2 = ma(Var20,len1) ;

}

condition1 = date == exitdate(1) And MarketPosition(1)== 1 ;

condition2 = date == exitdate(1) And MarketPosition(1)== -1 ;

If Var1<var2 Then

Var10=1 ;

Else

Var10=0 ;

If NthHighest(1,Var10,delay)==1 Then {

If time<150000 Then {

If condition1==False And high < dayopen + (dayhigh(1)-daylow(1))*len2 Then

buy("매수",Atstop,dayopen + (dayhigh(1)-daylow(1))*len2);

If condition2==False And low>dayopen-(dayhigh(1)-daylow(1))*len2 Then

sell("매도",Atstop,dayopen-(dayhigh(1)-daylow(1))*len2);

If condition1==False And high > dayopen + (dayhigh(1)-daylow(1))*len2 Then

buy("매수1",Atstop,NthHighest(1,high,delay));

If condition2==False And low < dayopen - (dayhigh(1)-daylow(1))*len2 Then

sell("매도1",Atstop,NthLowest(1,low,delay));

}

}

If MarketPosition <> 0 then {

exitlong("매수청산",Atstop,NthHighest(1,high, BarsSinceEntry+1)-atr(20)*s1);

exitshort("매도청산",Atstop,NthLowest(1,low, BarsSinceEntry+1)+atr(20)*s1) ;

}

- 1. DD_CongestionBreak.png (0.98 MB)

{kind=link}

답변 1

예스스탁 예스스탁 답변

2022-04-12 11:02:16

> 목포댁 님이 쓴 글입니다.

> 제목 : CT를 YT로 변환

> 수고하십니다.

공부목적으로 대신 CT 수식을 예트로 처음 변환하여 보았습니다.

pdf 파일인지라 복사붙이기가 깨끗하게 안나오는군요

무엇이 잘못되었는지 ,

변환된 예트 시스템식이 CT식과는 진입/청산이 틀리게 작동을 합니다

var1, var2를 장단기지표로 보고, CT지표로 나온 그림과 비교하였는데,

차트 세팅을 잘못한것인지(수정주가 on|off 둘 다 해봄) 차이가 좀 많이 나네요??!!!

아마도 CT함수와 YT함수 매칭이 잘못된 것 같은데, 체크 부탁 드립니다.

수정하신 부분에 기존소스 주석처리와 함께 설명도 부탁드리겠습니다.

그리고, 매수|매도와 매수1|매도1의 차이가 무엇인지요?

시간이 되면 원격접속 부탁 드리겠습니다.

#======================================================#

# CT <수식 0-11> DD_CongestionBreak(방법1)

#======================================================#

Input: len(10), len1(70), len2(0.37), s1(2.7), method(1), delay(8)

If method=1 Then

Var1=atr(len)

Var2=atr(len1)

Elseif method=2 Then

Var20=high-low

Var1=mov(Var20,len,s)

Var2=mov(Var20,len1,s)

End If

Cond1=tdate=exitdate(1) And position(1)=1

Cond2=tdate=exitdate(1) And position(1)=-1

If Var1<var2 Then

Var10=1

Else

Var10=0

EndIf

If hhv(1,Var10,delay)=1 Then

If ttime<1500 Then

If Cond1=False And high<opend+(highd(1)-lowd(1))*len2 Then

Call buy("매수",Atstop,Def,opend+(highd(1)-lowd(1))*len2)

End If

IfCond2=False And low>opend-(highd(1)-lowd(1))*len2 Then

Call sell("매도",Atstop,Def,opend-(highd(1)-lowd(1))*len2)

End If

If Cond1=False And high>opend+(highd(1)-lowd(1))*len2 Then

Call buy("매수1",Atstop,Def,hhv(1,high,delay))

End If

If Cond2=False And low<opend-(highd(1)-lowd(1))*len2 Then

Callsell("매도1",Atstop,Def,llv(1,low,delay))

End If

End if

End If

If position<>0then

Call exitlong("매수청산",Atstop,hhv(1,high,barnumsinceentry+1)-atr(20)*s1)

Call exitshort("매도청산",Atstop,llv(1,low,barnumsinceentry+1)+atr(20)*s1)

EndIf

#======================================================#

# YT <수식 0-11> DD_CongestionBreak(방법1)

#======================================================#

Input: len(10), len1(70), len2(0.37), s1(2.7), method(1), delay(8);

If method == 1 Then {

Var1=atr(len);

Var2=atr(len1) ;

}

Else if method == 2 Then {

Var20 = high - low;

Var1 = ma(Var20,len);

Var2 = ma(Var20,len1) ;

}

condition1 = date == exitdate(1) And MarketPosition(1)== 1 ;

condition2 = date == exitdate(1) And MarketPosition(1)== -1 ;

If Var1<var2 Then

Var10=1 ;

Else

Var10=0 ;

If NthHighest(1,Var10,delay)==1 Then {

If time<150000 Then {

If condition1==False And high < dayopen + (dayhigh(1)-daylow(1))*len2 Then

buy("매수",Atstop,dayopen + (dayhigh(1)-daylow(1))*len2);

If condition2==False And low>dayopen-(dayhigh(1)-daylow(1))*len2 Then

sell("매도",Atstop,dayopen-(dayhigh(1)-daylow(1))*len2);

If condition1==False And high > dayopen + (dayhigh(1)-daylow(1))*len2 Then

buy("매수1",Atstop,NthHighest(1,high,delay));

If condition2==False And low < dayopen - (dayhigh(1)-daylow(1))*len2 Then

sell("매도1",Atstop,NthLowest(1,low,delay));

}

}

If MarketPosition <> 0 then {

exitlong("매수청산",Atstop,NthHighest(1,high, BarsSinceEntry+1)-atr(20)*s1);

exitshort("매도청산",Atstop,NthLowest(1,low, BarsSinceEntry+1)+atr(20)*s1) ;

}

다음글

이전글