커뮤니티

수식어 부탁드립니다

2022-06-07 13:58:23

1103

글번호 159619

첨부 이미지

그림1

그림2

var : entry(0);

if Bdate != Bdate[1] Then

entry = 0;

if (MarketPosition != 0 and MarketPosition != MarketPosition[1]) or

(MarketPosition == MarketPosition[1] and TotalTrades > TotalTrades[1]) Then

entry = entry+1;

if entry < 1 then

{

input : 익절틱수(150),손절틱수(20);

if NextBarSdate != sDate Then

{

if NextBarOpen > C Then

Sell("s",AtStop,C);

if NextBarOpen < C Then

Buy("b",AtStop,C);

}

SetStopProfittarget(PriceScale*익절틱수,PointStop);

SetStopLoss(PriceScale*손절틱수,PointStop);

--------------

진입신호1회를 추가한 것인데요 수식어가 정확한지 문의드리고

추가로 매매시간은 08시40분부터 익일 05시00분의 수식어를 부탁드립니다.

------------------------------

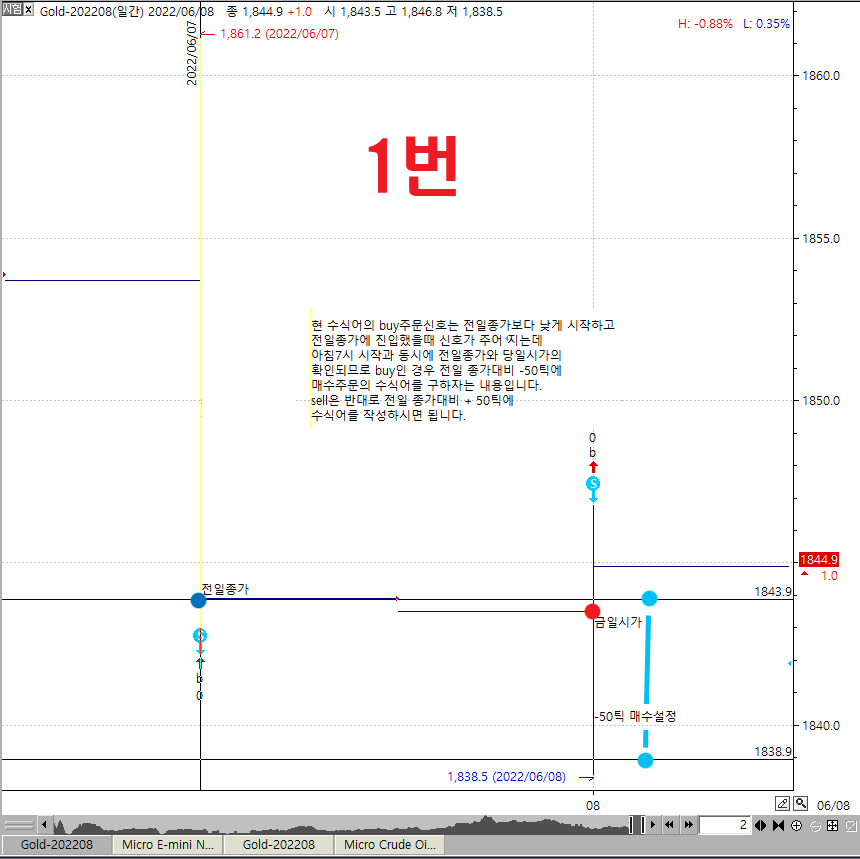

1번 그래프의 수식어 입니다.

input : 익절틱수(500),손절틱수(20);

if NextBarSdate != sDate Then

{

if NextBarOpen > C Then

Sell("s",AtStop,C);

if NextBarOpen < C Then

Buy("b",AtStop,C);

}

SetStopProfittarget(PriceScale*익절틱수,PointStop);

SetStopLoss(PriceScale*손절틱수,PointStop);

상기 수식어에 아래 내용을 추가로 부탁드립니다.

1. 진입신호1회

2. 매매시간을 한국시간 08시40분부터 익일 05시00분

3. 당일 7시시가 이후 전일종가~ 당일시가의 Buy,Sell 예상되는 진입신호값에서

자동주문이 (buy-50틱),(sell+50틱)에 되도록 부탁드립니다.

-----------------------------

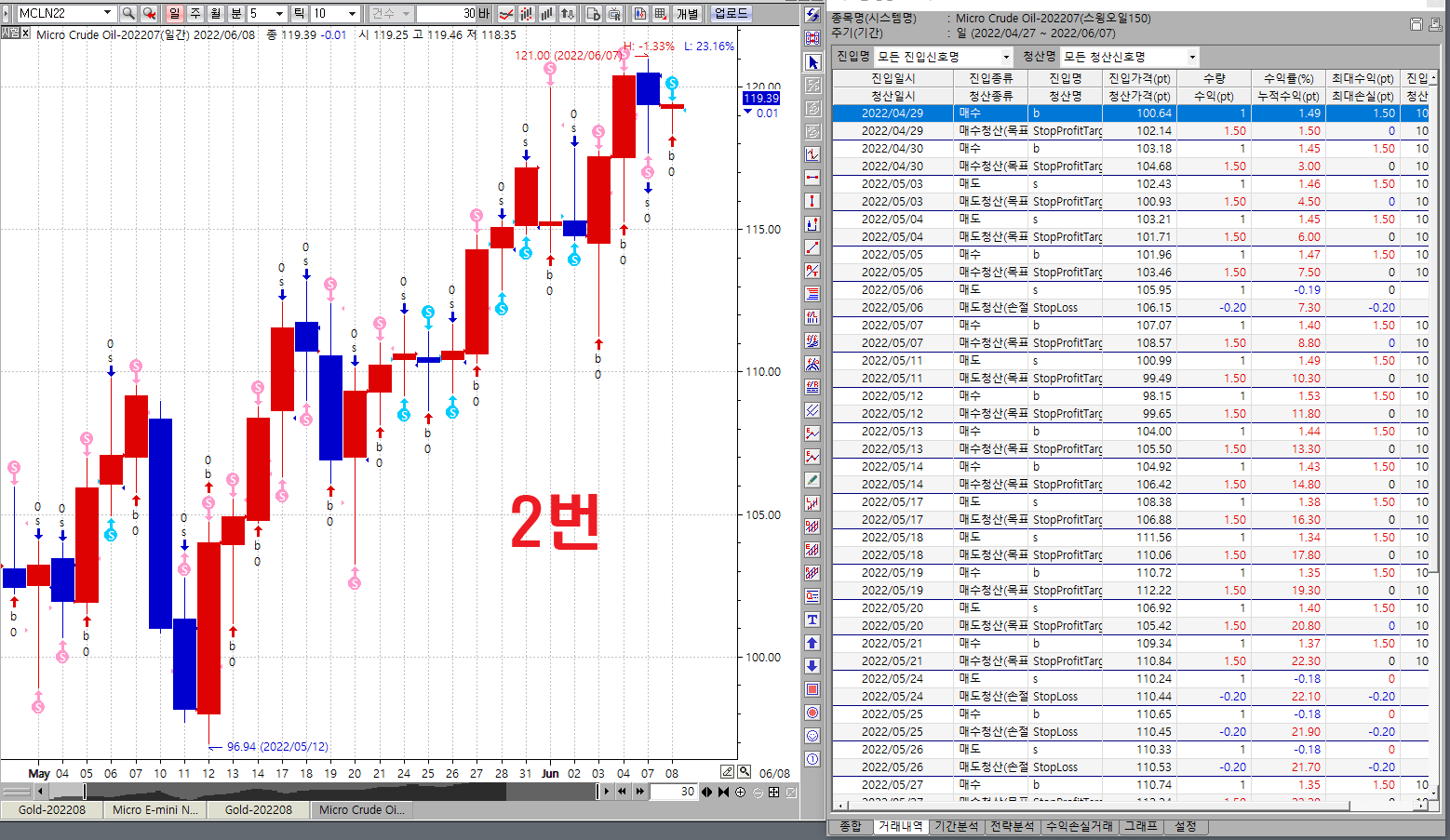

2번 그래프의 수식어 입니다.

input : 익절틱수(150),손절틱수(20);

if NextBarSdate != sDate Then

{

if NextBarOpen > C Then

Sell("s",AtStop,C);

if NextBarOpen < C Then

Buy("b",AtStop,C);

}

SetStopProfittarget(PriceScale*익절틱수,PointStop);

SetStopLoss(PriceScale*손절틱수,PointStop);

위는 제일 위 첨부파일의 수식어 입니다.

궁금한건 일봉매매에서 하루1회신호로 성능보고서 데이터로 나오는지 아니면 계속된 신호에 총합의 흐름으로 성능보고서가 나오는지 궁금합니다.

---------------------------------

- 1. 전시가.png (0.03 MB)

- 2. 160394_101010.png (0.11 MB)

{kind=link}

{kind=link}

답변 1

예스스탁 예스스탁 답변

2022-06-07 14:37:35

안녕하세요

예스스탁입니다.

1

랭귀지에서 하나의 buy나 sell은 한봉에 한번만 동작합니다.

수식에 buy와 sell이 하나씩만 사용되었고

올려주신 그림에서 차트 주기가 일봉이므로

하루에 매수진입과 매도진입이 한번씩만 동작하게 됩니다.

총 2회가 발생할 수 있습니다.

2

일봉차트에서는 시간을 조건으로 지정할 수 없습니다.

시간은 분단위 이하의 주기차트에서만 유효합니다.

그러므로 매매시간을 지정하시려면 분단위 이하의 주기에서

적용해야 하고 수식도 그에 맞게 변경하셔야 합니다.

3

또한 올리신 수식은 국내종목에나 사용되는 식입니다.

해외에도 일봉주기에서는 적용하셔도 되지만 분봉이하에서는 맞지 않는 내용이 됩니다.

국내종목은 야간시장이 없어 현재봉날짜와 다음봉시가날짜를 비교해서

날짜가 변경된것을 확인할 수 있지만

해외선물은 0시를 기준으로 영업일이 변경되지 않습니다.

4

수정한 식입니다. 분봉주기에 적용하셔야 합니다.

매수나 매도 중 먼저 만족한 것으로 1회만 진입하고

지정한 종료시간에 당일청산을 하게 됩니다.

input : 익절틱수(150),손절틱수(20);

input : StartTime(84000),EndTime(50000);

var : Tcond(false),entry(0);

IF Endtime > starttime Then

SetStopEndofday(Endtime);

Else

{

if sDate != sDate[1] Then

SetStopEndofday(Endtime);

}

if (sdate != sdate[1] and stime >= EndTime) or

(sdate == sdate[1] and stime >= EndTime and stime[1] < EndTime) Then

Tcond = False;

if (sdate != sdate[1] and stime >= StartTime) or

(sdate == sdate[1] and stime >= StartTime and stime[1] < StartTime) Then

{

Tcond = true;

IF Endtime <= starttime Then

{

SetStopEndofday(0);

}

}

if (NextBarSdate != sDate and NextBarStime >= 70000) or

(NextBarSdate == sDate and NextBarStime >= 70000 and sTime < 70000) Then

{

entry = 0;

if MarketPosition <= 0 Then

Sell("s",AtLimit,C+PriceScale*50);

if MarketPosition >= 0 Then

Buy("b",AtLimit,C-PriceScale*50);

}

if Tcond == true Then

{

if (MarketPosition != 0 and MarketPosition != MarketPosition[1]) or

(MarketPosition == MarketPosition[1] and TotalTrades > TotalTrades[1]) Then

entry = entry+1;

if MarketPosition <= 0 and entry < 1 and DayHigh < DayClose(1)+PriceScale*50 Then

Sell("s2",AtLimit,DayClose(1)+PriceScale*50);

if MarketPosition >= 0 and entry < 1 and DayLow > DayClose(1)-PriceScale*50 Then

Buy("b2",AtLimit,DayClose(1)-PriceScale*50);

}

SetStopProfittarget(PriceScale*익절틱수,PointStop);

SetStopLoss(PriceScale*손절틱수,PointStop);

즐거운 하루되세요

> 푸른 님이 쓴 글입니다.

> 제목 : 수식어 부탁드립니다

> var : entry(0);

if Bdate != Bdate[1] Then

entry = 0;

if (MarketPosition != 0 and MarketPosition != MarketPosition[1]) or

(MarketPosition == MarketPosition[1] and TotalTrades > TotalTrades[1]) Then

entry = entry+1;

if entry < 1 then

{

input : 익절틱수(150),손절틱수(20);

if NextBarSdate != sDate Then

{

if NextBarOpen > C Then

Sell("s",AtStop,C);

if NextBarOpen < C Then

Buy("b",AtStop,C);

}

SetStopProfittarget(PriceScale*익절틱수,PointStop);

SetStopLoss(PriceScale*손절틱수,PointStop);

--------------

진입신호1회를 추가한 것인데요 수식어가 정확한지 문의드리고

추가로 매매시간은 08시40분부터 익일 05시00분의 수식어를 부탁드립니다.

------------------------------

1번 그래프의 수식어 입니다.

input : 익절틱수(500),손절틱수(20);

if NextBarSdate != sDate Then

{

if NextBarOpen > C Then

Sell("s",AtStop,C);

if NextBarOpen < C Then

Buy("b",AtStop,C);

}

SetStopProfittarget(PriceScale*익절틱수,PointStop);

SetStopLoss(PriceScale*손절틱수,PointStop);

상기 수식어에 아래 내용을 추가로 부탁드립니다.

1. 진입신호1회

2. 매매시간을 한국시간 08시40분부터 익일 05시00분

3. 당일 7시시가 이후 전일종가~ 당일시가의 Buy,Sell 예상되는 진입신호값에서

자동주문이 (buy-50틱),(sell+50틱)에 되도록 부탁드립니다.

-----------------------------

2번 그래프의 수식어 입니다.

input : 익절틱수(150),손절틱수(20);

if NextBarSdate != sDate Then

{

if NextBarOpen > C Then

Sell("s",AtStop,C);

if NextBarOpen < C Then

Buy("b",AtStop,C);

}

SetStopProfittarget(PriceScale*익절틱수,PointStop);

SetStopLoss(PriceScale*손절틱수,PointStop);

위는 제일 위 첨부파일의 수식어 입니다.

궁금한건 일봉매매에서 하루1회신호로 성능보고서 데이터로 나오는지 아니면 계속된 신호에 총합의 흐름으로 성능보고서가 나오는지 궁금합니다.

---------------------------------

다음글

이전글