커뮤니티

문의 드립니다

2022-12-01 23:44:38

1408

글번호 164297

첨부 이미지

그림1

1.

input : starttime(120000),endtime(60000),n(30);

var : Tcond(false),hh(0),h1(0),ll(0),l1(0);

IF Endtime > starttime Then

SetStopEndofday(Endtime);

Else

{

if sDate != sDate[1] Then

SetStopEndofday(Endtime);

}

if (sdate != sdate[1] and stime >= endtime) or

(sdate == sdate[1] and stime >= endtime and stime[1] < endtime) then

{

Tcond = false;

}

if (sdate != sdate[1] and stime >= starttime) or

(sdate == sdate[1] and stime >= starttime and stime[1] < starttime) then

{

Tcond = true;

hh = h;

ll = l;

h1 = hh[1];

l1 = ll[1];

IF Endtime <= starttime Then

{

SetStopEndofday(0);

}

}

input : 익절틱수(0),손절틱수(30);

if NextBarOpen != C Then

{

Buy("b1",AtStop,NextBarOpen+PriceScale*10);

}

ExitLong("bx1",AtMarket);

if NextBarOpen != C Then

{

Sell("s1",AtStop,NextBarOpen-PriceScale*10);

}

ExitShort("sx1",AtMarket);

if NextBarSdate == sDate Then

{

if NextBarOpen == C Then

{

Buy("b2",AtStop,NextBarOpen+PriceScale*10);

}

}

ExitLong("bx2",AtMarket);

if NextBarOpen == C Then

{

Sell("s2",AtStop,NextBarOpen-PriceScale*10);

}

ExitShort("sx2",AtMarket);

SetStopProfittarget(PriceScale*익절틱수,PointStop);

SetStopLoss(PriceScale*손절틱수,PointStop);

-------------------------

2.

var1 = c-o;

Var2 = AccumN(var1,5);

input : starttime(120000),endtime(60000),n(0);

IF Endtime > starttime Then

SetStopEndofday(Endtime);

Else

{

if sDate != sDate[1] Then

SetStopEndofday(Endtime);

}

if (sdate != sdate[1] and stime >= endtime) or

(sdate == sdate[1] and stime >= endtime and stime[1] < endtime) then

{

IF Endtime <= starttime Then

{

SetStopEndofday(0);

}

}

if Var2 > 0 Then

Buy();

if var2 < 0 Then

Sell();

위 2가지 수식어를 240분봉 매매 자료로 사용하고 있습니다.

진입후 160틱 익절이나 240분봉의 완성시 청산되는 수식어를 추가할 수 없는지요 ?

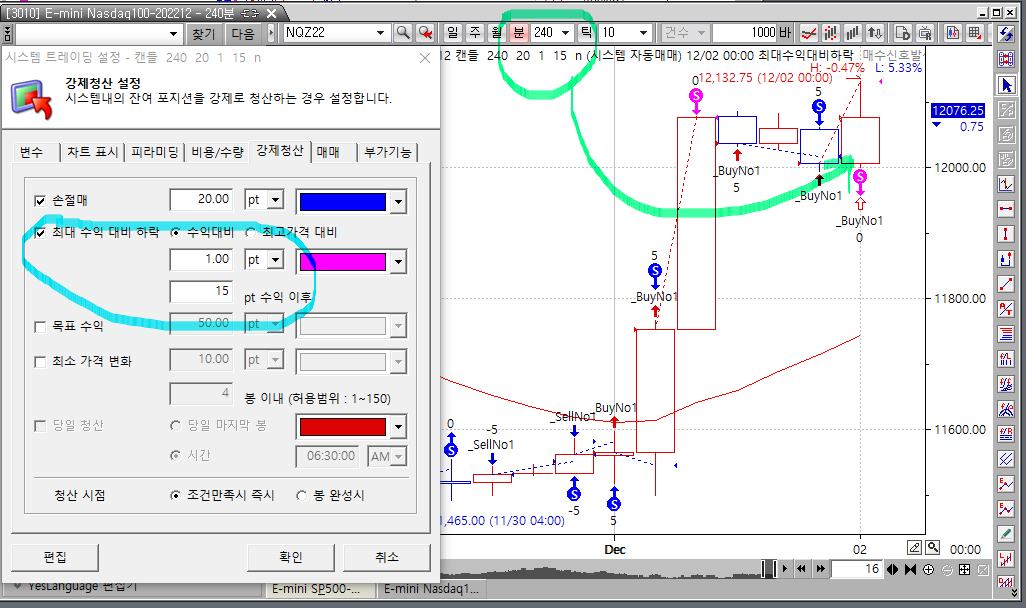

강제청산 설정에서 최대 수익대비 하락설정을 하게 되면 익절의 폭이 적게 나와서

질문 드려봅니다.

- 1. 165069_최대수익대비하락.png (0.07 MB)

{kind=link}

답변 1

예스스탁 예스스탁 답변

2022-12-02 10:02:54

안녕하세요

예스스탁입니다.

SetStopProfittarget(PriceScale*익절틱수,PointStop);

SetStopLoss(PriceScale*손절틱수,PointStop);

현재 1번수식에는 익절 손절수식이 있습니다.

외부변수로 틱수 지정하게 되어 있습니다.

1번식에는 봉완성시 청산추가,

2번식에는 익절과 봉완성시 청산을 추가해 드립니다.

1

input : starttime(120000),endtime(60000),n(30);

var : Tcond(false),hh(0),h1(0),ll(0),l1(0);

IF Endtime > starttime Then

SetStopEndofday(Endtime);

Else

{

if sDate != sDate[1] Then

SetStopEndofday(Endtime);

}

if (sdate != sdate[1] and stime >= endtime) or

(sdate == sdate[1] and stime >= endtime and stime[1] < endtime) then

{

Tcond = false;

}

if (sdate != sdate[1] and stime >= starttime) or

(sdate == sdate[1] and stime >= starttime and stime[1] < starttime) then

{

Tcond = true;

hh = h;

ll = l;

h1 = hh[1];

l1 = ll[1];

IF Endtime <= starttime Then

{

SetStopEndofday(0);

}

}

input : 익절틱수(160),손절틱수(30);

if NextBarOpen != C Then

{

Buy("b1",AtStop,NextBarOpen+PriceScale*10);

}

ExitLong("bx1",AtMarket);

if NextBarOpen != C Then

{

Sell("s1",AtStop,NextBarOpen-PriceScale*10);

}

ExitShort("sx1",AtMarket);

if NextBarSdate == sDate Then

{

if NextBarOpen == C Then

{

Buy("b2",AtStop,NextBarOpen+PriceScale*10);

}

}

ExitLong("bx2",AtMarket);

if NextBarOpen == C Then

{

Sell("s2",AtStop,NextBarOpen-PriceScale*10);

}

ExitShort("sx2",AtMarket);

SetStopProfittarget(PriceScale*익절틱수,PointStop);

SetStopLoss(PriceScale*손절틱수,PointStop);

ExitLong("bx");

ExitShort("sx");

2

input : starttime(120000),endtime(60000),n(0);

input : 익절틱수(160);

var1 = c-o;

Var2 = AccumN(var1,5);

IF Endtime > starttime Then

SetStopEndofday(Endtime);

Else

{

if sDate != sDate[1] Then

SetStopEndofday(Endtime);

}

if (sdate != sdate[1] and stime >= endtime) or

(sdate == sdate[1] and stime >= endtime and stime[1] < endtime) then

{

IF Endtime <= starttime Then

{

SetStopEndofday(0);

}

}

if Var2 > 0 Then

Buy();

if var2 < 0 Then

Sell();

SetStopProfittarget(PriceScale*익절틱수,PointStop);

ExitLong("bx");

ExitShort("sx");

즐거운 하루되세요

> 푸른 님이 쓴 글입니다.

> 제목 : 문의 드립니다

> 1.

input : starttime(120000),endtime(60000),n(30);

var : Tcond(false),hh(0),h1(0),ll(0),l1(0);

IF Endtime > starttime Then

SetStopEndofday(Endtime);

Else

{

if sDate != sDate[1] Then

SetStopEndofday(Endtime);

}

if (sdate != sdate[1] and stime >= endtime) or

(sdate == sdate[1] and stime >= endtime and stime[1] < endtime) then

{

Tcond = false;

}

if (sdate != sdate[1] and stime >= starttime) or

(sdate == sdate[1] and stime >= starttime and stime[1] < starttime) then

{

Tcond = true;

hh = h;

ll = l;

h1 = hh[1];

l1 = ll[1];

IF Endtime <= starttime Then

{

SetStopEndofday(0);

}

}

input : 익절틱수(0),손절틱수(30);

if NextBarOpen != C Then

{

Buy("b1",AtStop,NextBarOpen+PriceScale*10);

}

ExitLong("bx1",AtMarket);

if NextBarOpen != C Then

{

Sell("s1",AtStop,NextBarOpen-PriceScale*10);

}

ExitShort("sx1",AtMarket);

if NextBarSdate == sDate Then

{

if NextBarOpen == C Then

{

Buy("b2",AtStop,NextBarOpen+PriceScale*10);

}

}

ExitLong("bx2",AtMarket);

if NextBarOpen == C Then

{

Sell("s2",AtStop,NextBarOpen-PriceScale*10);

}

ExitShort("sx2",AtMarket);

SetStopProfittarget(PriceScale*익절틱수,PointStop);

SetStopLoss(PriceScale*손절틱수,PointStop);

-------------------------

2.

var1 = c-o;

Var2 = AccumN(var1,5);

input : starttime(120000),endtime(60000),n(0);

IF Endtime > starttime Then

SetStopEndofday(Endtime);

Else

{

if sDate != sDate[1] Then

SetStopEndofday(Endtime);

}

if (sdate != sdate[1] and stime >= endtime) or

(sdate == sdate[1] and stime >= endtime and stime[1] < endtime) then

{

IF Endtime <= starttime Then

{

SetStopEndofday(0);

}

}

if Var2 > 0 Then

Buy();

if var2 < 0 Then

Sell();

위 2가지 수식어를 240분봉 매매 자료로 사용하고 있습니다.

진입후 160틱 익절이나 240분봉의 완성시 청산되는 수식어를 추가할 수 없는지요 ?

강제청산 설정에서 최대 수익대비 하락설정을 하게 되면 익절의 폭이 적게 나와서

질문 드려봅니다.

다음글

이전글