커뮤니티

진입조건에 거래 후 청산하고 다시 진입조건에 거래하기 문의

2023-09-14 23:04:35

1805

글번호 172477

첨부 이미지

그림1

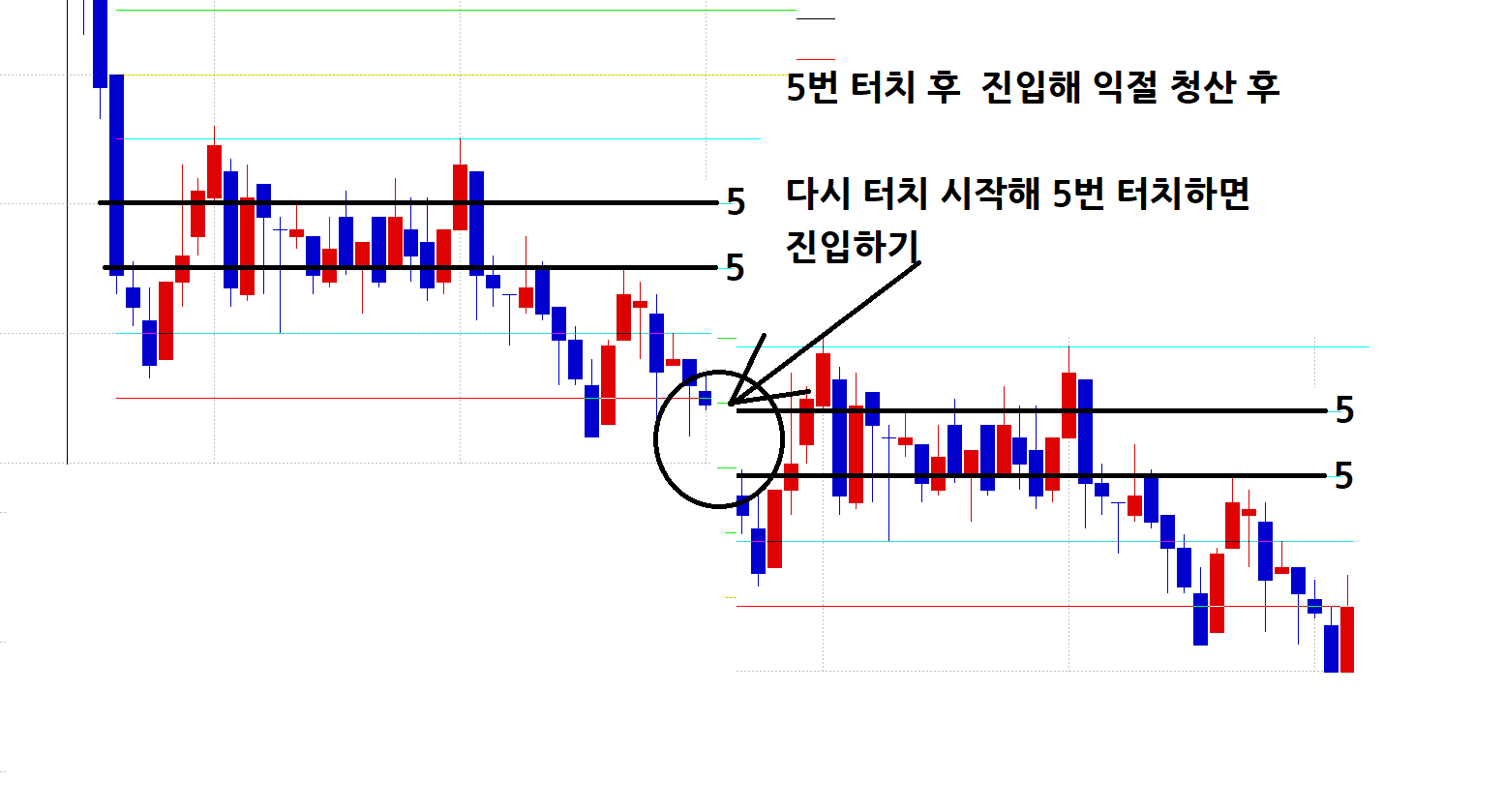

항상 도움에 감사드립니다.

이해를 돕기 위해 이미지를 첨부 했습니다.

아래의 수식은

여러 기준선들 중에서

상단이나 하단을 5번 먼저 터치 하면

진입이 시작되고 목표가격에서 청산 후

거래가 종료되는 수식인데요

--------------------------------------

input : ntime(173800), xtime(230000);

input : tick_size(8);

input : line_num(20); //줄을 몇개 그을 것인지

input : num(8); // 몇번 터치하면 진입하는지.

var : Tcond(False), oo(0), k(0), PriceScale_tick_size(0);

var : 상단(0),하단(0),n1(0),daypl(0),vol(0),xcond(False);

array : up_flag[100](0), dn_flag[100](0);

array : b_cnt[100](0), b_text_display[100](0);

array : b_b_cnt[100](0), b_b_text_display[100](0);

array : b_line[100](0), b_TL_display[100](0);

array : b_b_line[100](0), b_b_TL_display[100](0);

array : u_cnt[100](0), u_text_display[100](0);

array : u_u_cnt[100](0), u_u_text_display[100](0);

array : u_line[100](0), u_TL_display[100](0);

array : u_u_line[100](0), u_u_TL_display[100](0);

if (sdate != sdate[1] and stime >= xtime) or

(sdate == sdate[1] and stime >= xtime and stime[1] < xtime) Then

Tcond = False;

if (sdate != sdate[1] and stime >= ntime) or

(sdate == sdate[1] and stime >= ntime and stime[1] < ntime) Then

{

// 변수들 초기화 해주기

Tcond = true;

oo = o;

For k = 1 to line_num

{

up_flag[k] = 0;

dn_flag[k] = 0;

u_cnt[k] = 0;

u_u_cnt[k] = 0;

b_cnt[k] = 0;

b_b_cnt[k] = 0;

PriceScale_tick_size = PriceScale*tick_size;

u_line[k] = oo + (k-1)*PriceScale_tick_size;

u_u_line[k] = oo + k*PriceScale_tick_size;

b_line[k] = oo - (k-1)*PriceScale_tick_size;

b_b_line[k] = oo - k*PriceScale_tick_size;

}

// 조건문으로 터치 카운트 하기

For k = 1 to line_num

{

if H >= u_u_line[k] Then

{

up_flag[k] = 1;

u_u_cnt[k] = u_u_cnt[k] + 1;

}

if L <= b_b_line[k] Then

{

dn_flag[k] = -1;

b_b_cnt[k] = b_b_cnt[k] + 1;

}

}

}

Else

{

if Tcond == true Then

{

For k = 1 to line_num

{

if dn_flag[k] <= 0 and H >= b_line[k] and H[1] < b_line[k] Then

{

dn_flag[k] = 1;

b_cnt[k] = b_cnt[k] + 1;

}

if dn_flag[k] >= 0 and L <= b_b_line[k] and L[k] > b_b_line[k] Then

{

dn_flag[k] = -1;

b_b_cnt[k] = b_b_cnt[k] + 1;

}

if up_flag[k] <= 0 and H >= u_u_line[k] and H[1] < u_u_line[k] Then

{

up_flag[k] = 1;

u_u_cnt[k] = u_u_cnt[k] + 1;

}

if up_flag[k] >= 0 and L <= u_line[k] and L[1] > u_line[k] Then

{

up_flag[k] = -1;

u_cnt[k] = u_cnt[k] + 1;

}

}

}

}

var : T(0);

if (sdate != sdate[1] and stime >= ntime) or

(sdate == sdate[1] and stime >= ntime and stime[1] < ntime) Then

{

T = 0;

n1 = NetProfit;

xcond = False;

}

if TotalTrades > TotalTrades[1] and (IsExitName("bp3",1) or IsExitName("sp3",1)) Then

xcond = true;

if Tcond == true and xcond == False Then

{

if T == 0 Then

{

For k = 1 to line_num

{

if u_u_cnt[k] >= num or u_cnt[k] >= num Then

{

T = k;

상단 = u_u_line[k];

하단 = u_line[k];

}

if b_b_cnt[k] >= num or b_cnt[k] >= num Then

{

T = k;

상단 = b_line[k];

하단 = b_b_line[k];

}

}

}

if T != 0 Then

{

dayPL = (NetProfit-n1)+PositionProfit(0); // n1은 초기의 NetProfit이다.

if daypl >= 0 Then

vol = 2;

Else

vol = max(Ceiling(abs(daypl)/((상단-하단)*3)),2);

ClearDebug;

MessageLog("dayPL : %.2f | NetProfit : %.2f | PositionProfit : %.2f | vol : %.f", daypl, NetProfit, PositionProfit, vol);

MessageLog("상단 : %.2f | 하단 : %.2f | 위청산 : %.2f | 아래청산 : %.2f", 상단, 하단, 상단+(상단-하단)*6, 하단-(상단-하단)*6);

MessageLog("상단 - 하단 : %.2f, T : %.f", 상단-하단, T);

if MarketPosition <= 0 and CrossUp(C,상단) Then

Buy("b1",AtMarket,Def,vol);

if MarketPosition >= 0 and CrossDown(C,하단) Then

Sell("s1",AtMarket,Def,vol);

if MarketPosition == 1 Then

{

ExitLong("Bp1",AtLimit,상단+(상단-하단)*3,"",Floor(CurrentContracts*0.5),1); // 3배수 위치에서 물량 일부 청산하기, 1은 전체에서 한번 청산, 0은 각 진입 횟수 만큼 청산

ExitLong("Bp2",AtLimit,상단+(상단-하단)*7,"",Floor(CurrentContracts*0.5),1);

ExitLong("Bp3",AtLimit,상단+(상단-하단)*10);

}

if MarketPosition == -1 Then

{

ExitShort("sp1",AtLimit,하단-(상단-하단)*3,"",Floor(CurrentContracts*0.5),1);

ExitShort("sp2",AtLimit,하단-(상단-하단)*7,"",Floor(CurrentContracts*0.5),1);

ExitShort("sp3",AtLimit,하단-(상단-하단)*10);

}

MessageLog("daypl %.2f", daypl);

}

}

--------------------------------------------------------------

위의 수식을 아래와 같이 수정, 보완하고 싶습니다

1. 목표가에서 청산후 거래 종료 시점부터

2. 다시 터치 횟수를 처음부터 시작해 5번 터치하면

3. 처음 진입 조건과 같이 진입하고 목표가에서 청산하고

4. 또 목표가에서 청산하고 나면

5. 청산 시점부터 다시 터치 횟수를 시작해

6. 5번 터치 한곳에서 진입을 시작하는 수식입니다

도움 부탁드립니다

- 1. 173285_2023-09-12_21-40-14.png (0.03 MB)

{kind=link}

답변 2

예스스탁 예스스탁 답변

2023-09-15 10:39:13

안녕하세요

예스스탁입니다.

input : ntime(173800), xtime(230000);

input : tick_size(8);

input : line_num(20); //줄을 몇개 그을 것인지

input : num(8); // 몇번 터치하면 진입하는지.

var : Tcond(False), oo(0), k(0), PriceScale_tick_size(0);

var : 상단(0),하단(0),n1(0),daypl(0),vol(0),xcond(False);

array : up_flag[100](0), dn_flag[100](0);

array : b_cnt[100](0), b_text_display[100](0);

array : b_b_cnt[100](0), b_b_text_display[100](0);

array : b_line[100](0), b_TL_display[100](0);

array : b_b_line[100](0), b_b_TL_display[100](0);

array : u_cnt[100](0), u_text_display[100](0);

array : u_u_cnt[100](0), u_u_text_display[100](0);

array : u_line[100](0), u_TL_display[100](0);

array : u_u_line[100](0), u_u_TL_display[100](0);

if (sdate != sdate[1] and stime >= xtime) or

(sdate == sdate[1] and stime >= xtime and stime[1] < xtime) Then

Tcond = False;

if (sdate != sdate[1] and stime >= ntime) or

(sdate == sdate[1] and stime >= ntime and stime[1] < ntime) Then

{

// 변수들 초기화 해주기

Tcond = true;

oo = o;

For k = 1 to line_num

{

up_flag[k] = 0;

dn_flag[k] = 0;

u_cnt[k] = 0;

u_u_cnt[k] = 0;

b_cnt[k] = 0;

b_b_cnt[k] = 0;

PriceScale_tick_size = PriceScale*tick_size;

u_line[k] = oo + (k-1)*PriceScale_tick_size;

u_u_line[k] = oo + k*PriceScale_tick_size;

b_line[k] = oo - (k-1)*PriceScale_tick_size;

b_b_line[k] = oo - k*PriceScale_tick_size;

}

// 조건문으로 터치 카운트 하기

For k = 1 to line_num

{

if H >= u_u_line[k] Then

{

up_flag[k] = 1;

u_u_cnt[k] = u_u_cnt[k] + 1;

}

if L <= b_b_line[k] Then

{

dn_flag[k] = -1;

b_b_cnt[k] = b_b_cnt[k] + 1;

}

}

}

Else

{

if Tcond == true Then

{

if TotalTrades > TotalTrades[1] Then

{

oo = o;

For k = 1 to line_num

{

up_flag[k] = 0;

dn_flag[k] = 0;

u_cnt[k] = 0;

u_u_cnt[k] = 0;

b_cnt[k] = 0;

b_b_cnt[k] = 0;

PriceScale_tick_size = PriceScale*tick_size;

u_line[k] = oo + (k-1)*PriceScale_tick_size;

u_u_line[k] = oo + k*PriceScale_tick_size;

b_line[k] = oo - (k-1)*PriceScale_tick_size;

b_b_line[k] = oo - k*PriceScale_tick_size;

}

// 조건문으로 터치 카운트 하기

For k = 1 to line_num

{

if H >= u_u_line[k] Then

{

up_flag[k] = 1;

u_u_cnt[k] = u_u_cnt[k] + 1;

}

if L <= b_b_line[k] Then

{

dn_flag[k] = -1;

b_b_cnt[k] = b_b_cnt[k] + 1;

}

}

}

Else

{

For k = 1 to line_num

{

if dn_flag[k] <= 0 and H >= b_line[k] and H[1] < b_line[k] Then

{

dn_flag[k] = 1;

b_cnt[k] = b_cnt[k] + 1;

}

if dn_flag[k] >= 0 and L <= b_b_line[k] and L[k] > b_b_line[k] Then

{

dn_flag[k] = -1;

b_b_cnt[k] = b_b_cnt[k] + 1;

}

if up_flag[k] <= 0 and H >= u_u_line[k] and H[1] < u_u_line[k] Then

{

up_flag[k] = 1;

u_u_cnt[k] = u_u_cnt[k] + 1;

}

if up_flag[k] >= 0 and L <= u_line[k] and L[1] > u_line[k] Then

{

up_flag[k] = -1;

u_cnt[k] = u_cnt[k] + 1;

}

}

}

}

}

var : T(0);

if (sdate != sdate[1] and stime >= ntime) or

(sdate == sdate[1] and stime >= ntime and stime[1] < ntime) Then

{

T = 0;

n1 = NetProfit;

xcond = False;

}

if TotalTrades > TotalTrades[1] and (IsExitName("bp3",1) or IsExitName("sp3",1)) Then

xcond = true;

if Tcond == true and xcond == False Then

{

if T == 0 Then

{

For k = 1 to line_num

{

if u_u_cnt[k] >= num or u_cnt[k] >= num Then

{

T = k;

상단 = u_u_line[k];

하단 = u_line[k];

}

if b_b_cnt[k] >= num or b_cnt[k] >= num Then

{

T = k;

상단 = b_line[k];

하단 = b_b_line[k];

}

}

}

if T != 0 Then

{

dayPL = (NetProfit-n1)+PositionProfit(0); // n1은 초기의 NetProfit이다.

if daypl >= 0 Then

vol = 2;

Else

vol = max(Ceiling(abs(daypl)/((상단-하단)*3)),2);

ClearDebug;

MessageLog("dayPL : %.2f | NetProfit : %.2f | PositionProfit : %.2f | vol : %.f", daypl, NetProfit, PositionProfit, vol);

MessageLog("상단 : %.2f | 하단 : %.2f | 위청산 : %.2f | 아래청산 : %.2f", 상단, 하단, 상단+(상단-하단)*6, 하단-(상단-하단)*6);

MessageLog("상단 - 하단 : %.2f, T : %.f", 상단-하단, T);

if MarketPosition <= 0 and CrossUp(C,상단) Then

Buy("b1",AtMarket,Def,vol);

if MarketPosition >= 0 and CrossDown(C,하단) Then

Sell("s1",AtMarket,Def,vol);

if MarketPosition == 1 Then

{

ExitLong("Bp1",AtLimit,상단+(상단-하단)*3,"",Floor(CurrentContracts*0.5),1); // 3배수 위치에서 물량 일부 청산하기, 1은 전체에서 한번 청산, 0은 각 진입 횟수 만큼 청산

ExitLong("Bp2",AtLimit,상단+(상단-하단)*7,"",Floor(CurrentContracts*0.5),1);

ExitLong("Bp3",AtLimit,상단+(상단-하단)*10);

}

if MarketPosition == -1 Then

{

ExitShort("sp1",AtLimit,하단-(상단-하단)*3,"",Floor(CurrentContracts*0.5),1);

ExitShort("sp2",AtLimit,하단-(상단-하단)*7,"",Floor(CurrentContracts*0.5),1);

ExitShort("sp3",AtLimit,하단-(상단-하단)*10);

}

MessageLog("daypl %.2f", daypl);

}

}

즐거운 하루되세요

> 예스쟁이 님이 쓴 글입니다.

> 제목 : 진입조건에 거래 후 청산하고 다시 진입조건에 거래하기 문의

> 항상 도움에 감사드립니다.

이해를 돕기 위해 이미지를 첨부 했습니다.

아래의 수식은

여러 기준선들 중에서

상단이나 하단을 5번 먼저 터치 하면

진입이 시작되고 목표가격에서 청산 후

거래가 종료되는 수식인데요

--------------------------------------

input : ntime(173800), xtime(230000);

input : tick_size(8);

input : line_num(20); //줄을 몇개 그을 것인지

input : num(8); // 몇번 터치하면 진입하는지.

var : Tcond(False), oo(0), k(0), PriceScale_tick_size(0);

var : 상단(0),하단(0),n1(0),daypl(0),vol(0),xcond(False);

array : up_flag[100](0), dn_flag[100](0);

array : b_cnt[100](0), b_text_display[100](0);

array : b_b_cnt[100](0), b_b_text_display[100](0);

array : b_line[100](0), b_TL_display[100](0);

array : b_b_line[100](0), b_b_TL_display[100](0);

array : u_cnt[100](0), u_text_display[100](0);

array : u_u_cnt[100](0), u_u_text_display[100](0);

array : u_line[100](0), u_TL_display[100](0);

array : u_u_line[100](0), u_u_TL_display[100](0);

if (sdate != sdate[1] and stime >= xtime) or

(sdate == sdate[1] and stime >= xtime and stime[1] < xtime) Then

Tcond = False;

if (sdate != sdate[1] and stime >= ntime) or

(sdate == sdate[1] and stime >= ntime and stime[1] < ntime) Then

{

// 변수들 초기화 해주기

Tcond = true;

oo = o;

For k = 1 to line_num

{

up_flag[k] = 0;

dn_flag[k] = 0;

u_cnt[k] = 0;

u_u_cnt[k] = 0;

b_cnt[k] = 0;

b_b_cnt[k] = 0;

PriceScale_tick_size = PriceScale*tick_size;

u_line[k] = oo + (k-1)*PriceScale_tick_size;

u_u_line[k] = oo + k*PriceScale_tick_size;

b_line[k] = oo - (k-1)*PriceScale_tick_size;

b_b_line[k] = oo - k*PriceScale_tick_size;

}

// 조건문으로 터치 카운트 하기

For k = 1 to line_num

{

if H >= u_u_line[k] Then

{

up_flag[k] = 1;

u_u_cnt[k] = u_u_cnt[k] + 1;

}

if L <= b_b_line[k] Then

{

dn_flag[k] = -1;

b_b_cnt[k] = b_b_cnt[k] + 1;

}

}

}

Else

{

if Tcond == true Then

{

For k = 1 to line_num

{

if dn_flag[k] <= 0 and H >= b_line[k] and H[1] < b_line[k] Then

{

dn_flag[k] = 1;

b_cnt[k] = b_cnt[k] + 1;

}

if dn_flag[k] >= 0 and L <= b_b_line[k] and L[k] > b_b_line[k] Then

{

dn_flag[k] = -1;

b_b_cnt[k] = b_b_cnt[k] + 1;

}

if up_flag[k] <= 0 and H >= u_u_line[k] and H[1] < u_u_line[k] Then

{

up_flag[k] = 1;

u_u_cnt[k] = u_u_cnt[k] + 1;

}

if up_flag[k] >= 0 and L <= u_line[k] and L[1] > u_line[k] Then

{

up_flag[k] = -1;

u_cnt[k] = u_cnt[k] + 1;

}

}

}

}

var : T(0);

if (sdate != sdate[1] and stime >= ntime) or

(sdate == sdate[1] and stime >= ntime and stime[1] < ntime) Then

{

T = 0;

n1 = NetProfit;

xcond = False;

}

if TotalTrades > TotalTrades[1] and (IsExitName("bp3",1) or IsExitName("sp3",1)) Then

xcond = true;

if Tcond == true and xcond == False Then

{

if T == 0 Then

{

For k = 1 to line_num

{

if u_u_cnt[k] >= num or u_cnt[k] >= num Then

{

T = k;

상단 = u_u_line[k];

하단 = u_line[k];

}

if b_b_cnt[k] >= num or b_cnt[k] >= num Then

{

T = k;

상단 = b_line[k];

하단 = b_b_line[k];

}

}

}

if T != 0 Then

{

dayPL = (NetProfit-n1)+PositionProfit(0); // n1은 초기의 NetProfit이다.

if daypl >= 0 Then

vol = 2;

Else

vol = max(Ceiling(abs(daypl)/((상단-하단)*3)),2);

ClearDebug;

MessageLog("dayPL : %.2f | NetProfit : %.2f | PositionProfit : %.2f | vol : %.f", daypl, NetProfit, PositionProfit, vol);

MessageLog("상단 : %.2f | 하단 : %.2f | 위청산 : %.2f | 아래청산 : %.2f", 상단, 하단, 상단+(상단-하단)*6, 하단-(상단-하단)*6);

MessageLog("상단 - 하단 : %.2f, T : %.f", 상단-하단, T);

if MarketPosition <= 0 and CrossUp(C,상단) Then

Buy("b1",AtMarket,Def,vol);

if MarketPosition >= 0 and CrossDown(C,하단) Then

Sell("s1",AtMarket,Def,vol);

if MarketPosition == 1 Then

{

ExitLong("Bp1",AtLimit,상단+(상단-하단)*3,"",Floor(CurrentContracts*0.5),1); // 3배수 위치에서 물량 일부 청산하기, 1은 전체에서 한번 청산, 0은 각 진입 횟수 만큼 청산

ExitLong("Bp2",AtLimit,상단+(상단-하단)*7,"",Floor(CurrentContracts*0.5),1);

ExitLong("Bp3",AtLimit,상단+(상단-하단)*10);

}

if MarketPosition == -1 Then

{

ExitShort("sp1",AtLimit,하단-(상단-하단)*3,"",Floor(CurrentContracts*0.5),1);

ExitShort("sp2",AtLimit,하단-(상단-하단)*7,"",Floor(CurrentContracts*0.5),1);

ExitShort("sp3",AtLimit,하단-(상단-하단)*10);

}

MessageLog("daypl %.2f", daypl);

}

}

--------------------------------------------------------------

위의 수식을 아래와 같이 수정, 보완하고 싶습니다

1. 목표가에서 청산후 거래 종료 시점부터

2. 다시 터치 횟수를 처음부터 시작해 5번 터치하면

3. 처음 진입 조건과 같이 진입하고 목표가에서 청산하고

4. 또 목표가에서 청산하고 나면

5. 청산 시점부터 다시 터치 횟수를 시작해

6. 5번 터치 한곳에서 진입을 시작하는 수식입니다

도움 부탁드립니다

예스쟁이

2023-09-15 20:20:40

답변에 감사드립니다.

답변주신 수식 중에 궁금한 부분이 있어서 추가 문의 드립니다.

----------------------------------------------

if TotalTrades > TotalTrades[1] Then

---------------------------------------------

위의 부분에서 TotalTrades 는

청산 완료된 전체 거래의 횟수라고 알고 있는데요.

어떤 상황에 위의 조건문이 실행되는건지

알고 싶습니다.

해석 부탁드립니다.