커뮤니티

검토 부탁드립니다.

2013-09-24 21:15:15

166

글번호 67777

첨부 이미지

그림1

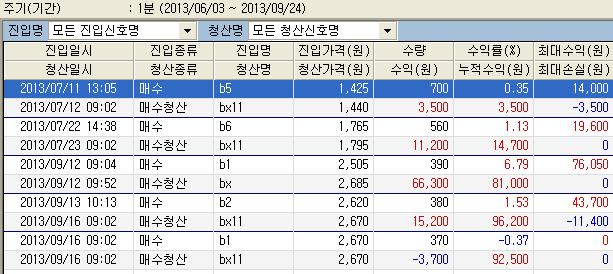

시뮬레이션 해 봤는데요.

9월 16일, 09:02시에 청산되었는데..

또 매수되고 다시 청산되는 현상이 있습니다.

사진 한번 봐주십시요.

*오늘 청산되어다면, 오늘은 매수금지가 되야 합니다.

===============================

input : P(5);

var : cnt(0),sum(0),sum1(0),mav(0),mav1(0),dis(0),dis1(0),daycnt(0),PredayVol(0);

Var : Pivot(0),R1(0),R2(0),S1(0),S2(0);

var : 상한가(0), UpLimit(0);

var : up1(0), up2(0), up3(0), up4(0), up5(0),up6(0);

if date >= 19981207 then {

if date < 20050328 && CodeCategory() == 2 then

UpLimit = (BP[0] * 1.12);

Else

UpLimit = (BP[0] * 1.15);

if CodeCategory() == 2 then {

if date >= 20030721 then {

up1 = int(UpLimit/100+0.00001)*100;

up2 = int(UpLimit/100+0.00001)*100;

up3 = int(UpLimit/100+0.00001)*100;

up4 = int(UpLimit/50+0.00001)*50;

up5 = int(UpLimit/10+0.00001)*10;

up6 = int(UpLimit/5+0.00001)*5;

}

else {

up1 = int(UpLimit/1000+0.00001)*1000;

up2 = int(UpLimit/500+0.00001)*500;

up3 = int(UpLimit/100+0.00001)*100;

up4 = int(UpLimit/50+0.00001)*50;

up5 = int(UpLimit/10+0.00001)*10;

up6 = int(UpLimit/10+0.00001)*10;

}

}

Else {

up1 = int(UpLimit/1000+0.00001)*1000;

up2 = int(UpLimit/500+0.00001)*500;

up3 = int(UpLimit/100+0.00001)*100;

up4 = int(UpLimit/50+0.00001)*50;

up5 = int(UpLimit/10+0.00001)*10;

up6 = int(UpLimit/5+0.00001)*5;

}

if CodeCategory() == 1 || CodeCategory() == 2 then {

If BP >= 500000 Then

상한가 = up1;

Else If BP >= 100000 Then

상한가 = iff(up2>=500000, up1, up2);

Else If BP >= 50000 Then

상한가 = iff(up3>=100000, up2, up3);

Else If BP >= 10000 Then

상한가 = iff(up4>=50000, up3, up4);

Else If BP >= 5000 Then

상한가 = iff(up5>=10000, up4, up5);

Else

상한가 = iff(up6>=5000, up5, up6);

}

else if CodeCategory() == 8 || CodeCategory() == 9 then { // ETF

상한가 = up6;

}

}

value1 = 상한가;

Pivot = (DayHigh(1)+DayLow(1)+DayClose(1))/3;

sum = 0;

sum1 = 0;

for cnt = 0 to P-1{

sum = sum+DayClose(cnt);

sum1 = sum1+DayClose(cnt+1);

}

mav = sum/P;

mav1 = sum1/P;

dis = c/mav*100;

dis1 = DayClose(1)/mav1*100;

for cnt = 1 to 1000 {

if stime == stime[cnt] and sdate != sdate[cnt] then{

PredayVol = DayVolume[cnt];

cnt = 1001;

}

}

if date != date[1] Then{

Daycnt = daycnt+1;

var1 = dayopen/mav*100;

value2 = value1[1];

value3 = value2[1];

value4 = value3[1];

value5 = value4[1];

}

#5일 상한가 평균

value99 = (value1+value2+value3+value4+value5)/5;

if dayopen <= DayClose(1)*1.01 and

dayhigh <= dayopen*1.04 and

dis1 >= 103 and

ExitDate(1) != sdate and

DayVolume < PredayVol*1 and

var1 > 100 Then{

if stime >= 90000 and stime < 100000 and dis >= 100.5 and dis < 101.5 Then

buy("b1",AtMarket);

if stime >= 100000 and stime < 110000 and dis >= 100.5 and dis < 102.0 Then

buy("b2",AtMarket);

if stime >= 110000 and stime < 120000 and dis >= 100.5 and dis < 102.5 Then

buy("b3",AtMarket);

if stime >= 120000 and stime < 130000 and dis >= 100.5 and dis < 103.0 Then

buy("b4",AtMarket);

if stime >= 130000 and stime < 140000 and dis >= 100.5 and dis < 103.5 Then

buy("b5",AtMarket);

if stime >= 140000 and stime < 144800 and dis >= 100.5 and dis < 104.0 Then

buy("b6",AtMarket);

if stime >= 143000 and stime < 144800 and c < Pivot and dis >= 100.5 and dis < 104.5 Then

buy("b7",AtMarket);

}

if MarketPosition == 1 Then{

if C <= EntryPrice*0.945 Then

ExitLong("x",AtMarket);

if sdate == EntryDate and C >= EntryPrice*1.06 Then

ExitLong("bx",AtMarket);

if sdate > EntryDate and daycnt == daycnt[BarsSinceEntry]+1 and dayopen < value99 Then{

if stime >= 090000 and stime <= 093000 and C >= EntryPrice*1.01 Then

ExitLong("bx11",AtMarket);

if stime >= 093100 and stime <= 100000 and CrossUp(C,EntryPrice) Then

ExitLong("bx12",AtMarket);

if stime > 100000 Then

ExitLong("bx13",AtMarket);

}

if sdate > EntryDate and daycnt == daycnt[BarsSinceEntry]+1 and dayopen > value99 Then{

if C <= value99-PriceScale*2 Then

ExitLong("bx21",AtMarket);

if C >= EntryPrice*1.10 Then

ExitLong("bx22",AtMarket);

if C >= dayopen*1.075 Then

ExitLong("bx23",AtMarket);

}

if sdate > EntryDate and daycnt == daycnt[BarsSinceEntry]+2 Then{

if C >= EntryPrice*1.15 Then

ExitLong("bx31",AtMarket);

if C >= DayOpen*1.10 Then

ExitLong("bx32",AtMarket);

if stime >= 94000 Then

ExitLong("bx33",AtMarket);

}

}

- 1. 매도당일_매수.1.JPG (0.05 MB)

{kind=link}

답변 1

예스스탁 예스스탁 답변

2013-09-25 14:42:06

안녕하세요

예스스탁입니다.

수정한 식입니다.

input : P(5);

var : cnt(0),sum(0),sum1(0),mav(0),mav1(0),dis(0),dis1(0),daycnt(0),PredayVol(0);

Var : Pivot(0),R1(0),R2(0),S1(0),S2(0);

var : 상한가(0), UpLimit(0);

var : up1(0), up2(0), up3(0), up4(0), up5(0),up6(0);

if date >= 19981207 then {

if date < 20050328 && CodeCategory() == 2 then

UpLimit = (BP[0] * 1.12);

Else

UpLimit = (BP[0] * 1.15);

if CodeCategory() == 2 then {

if date >= 20030721 then {

up1 = int(UpLimit/100+0.00001)*100;

up2 = int(UpLimit/100+0.00001)*100;

up3 = int(UpLimit/100+0.00001)*100;

up4 = int(UpLimit/50+0.00001)*50;

up5 = int(UpLimit/10+0.00001)*10;

up6 = int(UpLimit/5+0.00001)*5;

}

else {

up1 = int(UpLimit/1000+0.00001)*1000;

up2 = int(UpLimit/500+0.00001)*500;

up3 = int(UpLimit/100+0.00001)*100;

up4 = int(UpLimit/50+0.00001)*50;

up5 = int(UpLimit/10+0.00001)*10;

up6 = int(UpLimit/10+0.00001)*10;

}

}

Else {

up1 = int(UpLimit/1000+0.00001)*1000;

up2 = int(UpLimit/500+0.00001)*500;

up3 = int(UpLimit/100+0.00001)*100;

up4 = int(UpLimit/50+0.00001)*50;

up5 = int(UpLimit/10+0.00001)*10;

up6 = int(UpLimit/5+0.00001)*5;

}

if CodeCategory() == 1 || CodeCategory() == 2 then {

If BP >= 500000 Then

상한가 = up1;

Else If BP >= 100000 Then

상한가 = iff(up2>=500000, up1, up2);

Else If BP >= 50000 Then

상한가 = iff(up3>=100000, up2, up3);

Else If BP >= 10000 Then

상한가 = iff(up4>=50000, up3, up4);

Else If BP >= 5000 Then

상한가 = iff(up5>=10000, up4, up5);

Else

상한가 = iff(up6>=5000, up5, up6);

}

else if CodeCategory() == 8 || CodeCategory() == 9 then { // ETF

상한가 = up6;

}

}

value1 = 상한가;

Pivot = (DayHigh(1)+DayLow(1)+DayClose(1))/3;

sum = 0;

sum1 = 0;

for cnt = 0 to P-1{

sum = sum+DayClose(cnt);

sum1 = sum1+DayClose(cnt+1);

}

mav = sum/P;

mav1 = sum1/P;

dis = c/mav*100;

dis1 = DayClose(1)/mav1*100;

for cnt = 1 to 1000 {

if stime == stime[cnt] and sdate != sdate[cnt] then{

PredayVol = DayVolume[cnt];

cnt = 1001;

}

}

if date != date[1] Then{

Daycnt = daycnt+1;

var1 = dayopen/mav*100;

value2 = value1[1];

value3 = value2[1];

value4 = value3[1];

value5 = value4[1];

}

#5일 상한가 평균

value99 = (value1+value2+value3+value4+value5)/5;

if MarketPosition == 0 and

dayopen <= DayClose(1)*1.01 and

dayhigh <= dayopen*1.04 and

dis1 >= 103 and

ExitDate(1) != sdate and

DayVolume < PredayVol*1 and

var1 > 100 Then{

if stime >= 90000 and stime < 100000 and dis >= 100.5 and dis < 101.5 Then

buy("b1",AtMarket);

if stime >= 100000 and stime < 110000 and dis >= 100.5 and dis < 102.0 Then

buy("b2",AtMarket);

if stime >= 110000 and stime < 120000 and dis >= 100.5 and dis < 102.5 Then

buy("b3",AtMarket);

if stime >= 120000 and stime < 130000 and dis >= 100.5 and dis < 103.0 Then

buy("b4",AtMarket);

if stime >= 130000 and stime < 140000 and dis >= 100.5 and dis < 103.5 Then

buy("b5",AtMarket);

if stime >= 140000 and stime < 144800 and dis >= 100.5 and dis < 104.0 Then

buy("b6",AtMarket);

if stime >= 143000 and stime < 144800 and c < Pivot and dis >= 100.5 and dis < 104.5 Then

buy("b7",AtMarket);

}

if MarketPosition == 1 Then{

if C <= EntryPrice*0.945 Then

ExitLong("x",AtMarket);

if sdate == EntryDate and C >= EntryPrice*1.06 Then

ExitLong("bx",AtMarket);

if sdate > EntryDate and daycnt == daycnt[BarsSinceEntry]+1 and dayopen < value99 Then{

if stime >= 090000 and stime <= 093000 and C >= EntryPrice*1.01 Then

ExitLong("bx11",AtMarket);

if stime >= 093100 and stime <= 100000 and CrossUp(C,EntryPrice) Then

ExitLong("bx12",AtMarket);

if stime > 100000 Then

ExitLong("bx13",AtMarket);

}

if sdate > EntryDate and daycnt == daycnt[BarsSinceEntry]+1 and dayopen > value99 Then{

if C <= value99-PriceScale*2 Then

ExitLong("bx21",AtMarket);

if C >= EntryPrice*1.10 Then

ExitLong("bx22",AtMarket);

if C >= dayopen*1.075 Then

ExitLong("bx23",AtMarket);

}

if sdate > EntryDate and daycnt == daycnt[BarsSinceEntry]+2 Then{

if C >= EntryPrice*1.15 Then

ExitLong("bx31",AtMarket);

if C >= DayOpen*1.10 Then

ExitLong("bx32",AtMarket);

if stime >= 94000 Then

ExitLong("bx33",AtMarket);

}

}

즐거운 하루되세요

> 쌀사비팔 님이 쓴 글입니다.

> 제목 : 검토 부탁드립니다.

> 시뮬레이션 해 봤는데요.

9월 16일, 09:02시에 청산되었는데..

또 매수되고 다시 청산되는 현상이 있습니다.

사진 한번 봐주십시요.

*오늘 청산되어다면, 오늘은 매수금지가 되야 합니다.

===============================

input : P(5);

var : cnt(0),sum(0),sum1(0),mav(0),mav1(0),dis(0),dis1(0),daycnt(0),PredayVol(0);

Var : Pivot(0),R1(0),R2(0),S1(0),S2(0);

var : 상한가(0), UpLimit(0);

var : up1(0), up2(0), up3(0), up4(0), up5(0),up6(0);

if date >= 19981207 then {

if date < 20050328 && CodeCategory() == 2 then

UpLimit = (BP[0] * 1.12);

Else

UpLimit = (BP[0] * 1.15);

if CodeCategory() == 2 then {

if date >= 20030721 then {

up1 = int(UpLimit/100+0.00001)*100;

up2 = int(UpLimit/100+0.00001)*100;

up3 = int(UpLimit/100+0.00001)*100;

up4 = int(UpLimit/50+0.00001)*50;

up5 = int(UpLimit/10+0.00001)*10;

up6 = int(UpLimit/5+0.00001)*5;

}

else {

up1 = int(UpLimit/1000+0.00001)*1000;

up2 = int(UpLimit/500+0.00001)*500;

up3 = int(UpLimit/100+0.00001)*100;

up4 = int(UpLimit/50+0.00001)*50;

up5 = int(UpLimit/10+0.00001)*10;

up6 = int(UpLimit/10+0.00001)*10;

}

}

Else {

up1 = int(UpLimit/1000+0.00001)*1000;

up2 = int(UpLimit/500+0.00001)*500;

up3 = int(UpLimit/100+0.00001)*100;

up4 = int(UpLimit/50+0.00001)*50;

up5 = int(UpLimit/10+0.00001)*10;

up6 = int(UpLimit/5+0.00001)*5;

}

if CodeCategory() == 1 || CodeCategory() == 2 then {

If BP >= 500000 Then

상한가 = up1;

Else If BP >= 100000 Then

상한가 = iff(up2>=500000, up1, up2);

Else If BP >= 50000 Then

상한가 = iff(up3>=100000, up2, up3);

Else If BP >= 10000 Then

상한가 = iff(up4>=50000, up3, up4);

Else If BP >= 5000 Then

상한가 = iff(up5>=10000, up4, up5);

Else

상한가 = iff(up6>=5000, up5, up6);

}

else if CodeCategory() == 8 || CodeCategory() == 9 then { // ETF

상한가 = up6;

}

}

value1 = 상한가;

Pivot = (DayHigh(1)+DayLow(1)+DayClose(1))/3;

sum = 0;

sum1 = 0;

for cnt = 0 to P-1{

sum = sum+DayClose(cnt);

sum1 = sum1+DayClose(cnt+1);

}

mav = sum/P;

mav1 = sum1/P;

dis = c/mav*100;

dis1 = DayClose(1)/mav1*100;

for cnt = 1 to 1000 {

if stime == stime[cnt] and sdate != sdate[cnt] then{

PredayVol = DayVolume[cnt];

cnt = 1001;

}

}

if date != date[1] Then{

Daycnt = daycnt+1;

var1 = dayopen/mav*100;

value2 = value1[1];

value3 = value2[1];

value4 = value3[1];

value5 = value4[1];

}

#5일 상한가 평균

value99 = (value1+value2+value3+value4+value5)/5;

if dayopen <= DayClose(1)*1.01 and

dayhigh <= dayopen*1.04 and

dis1 >= 103 and

ExitDate(1) != sdate and

DayVolume < PredayVol*1 and

var1 > 100 Then{

if stime >= 90000 and stime < 100000 and dis >= 100.5 and dis < 101.5 Then

buy("b1",AtMarket);

if stime >= 100000 and stime < 110000 and dis >= 100.5 and dis < 102.0 Then

buy("b2",AtMarket);

if stime >= 110000 and stime < 120000 and dis >= 100.5 and dis < 102.5 Then

buy("b3",AtMarket);

if stime >= 120000 and stime < 130000 and dis >= 100.5 and dis < 103.0 Then

buy("b4",AtMarket);

if stime >= 130000 and stime < 140000 and dis >= 100.5 and dis < 103.5 Then

buy("b5",AtMarket);

if stime >= 140000 and stime < 144800 and dis >= 100.5 and dis < 104.0 Then

buy("b6",AtMarket);

if stime >= 143000 and stime < 144800 and c < Pivot and dis >= 100.5 and dis < 104.5 Then

buy("b7",AtMarket);

}

if MarketPosition == 1 Then{

if C <= EntryPrice*0.945 Then

ExitLong("x",AtMarket);

if sdate == EntryDate and C >= EntryPrice*1.06 Then

ExitLong("bx",AtMarket);

if sdate > EntryDate and daycnt == daycnt[BarsSinceEntry]+1 and dayopen < value99 Then{

if stime >= 090000 and stime <= 093000 and C >= EntryPrice*1.01 Then

ExitLong("bx11",AtMarket);

if stime >= 093100 and stime <= 100000 and CrossUp(C,EntryPrice) Then

ExitLong("bx12",AtMarket);

if stime > 100000 Then

ExitLong("bx13",AtMarket);

}

if sdate > EntryDate and daycnt == daycnt[BarsSinceEntry]+1 and dayopen > value99 Then{

if C <= value99-PriceScale*2 Then

ExitLong("bx21",AtMarket);

if C >= EntryPrice*1.10 Then

ExitLong("bx22",AtMarket);

if C >= dayopen*1.075 Then

ExitLong("bx23",AtMarket);

}

if sdate > EntryDate and daycnt == daycnt[BarsSinceEntry]+2 Then{

if C >= EntryPrice*1.15 Then

ExitLong("bx31",AtMarket);

if C >= DayOpen*1.10 Then

ExitLong("bx32",AtMarket);

if stime >= 94000 Then

ExitLong("bx33",AtMarket);

}

}

이전글